In the modern financial sector, the exponential growth of data has made

efficient and accurate financial data analysis increasingly crucial.

Traditional methods, such as statistical analysis and rule-based systems, often

struggle to process and derive meaningful insights from complex financial

information effectively. These conventional approaches face inherent

limitations in handling unstructured data, capturing intricate market patterns,

and adapting to rapidly evolving financial contexts, resulting in reduced

accuracy and delayed decision-making processes. To address these challenges,

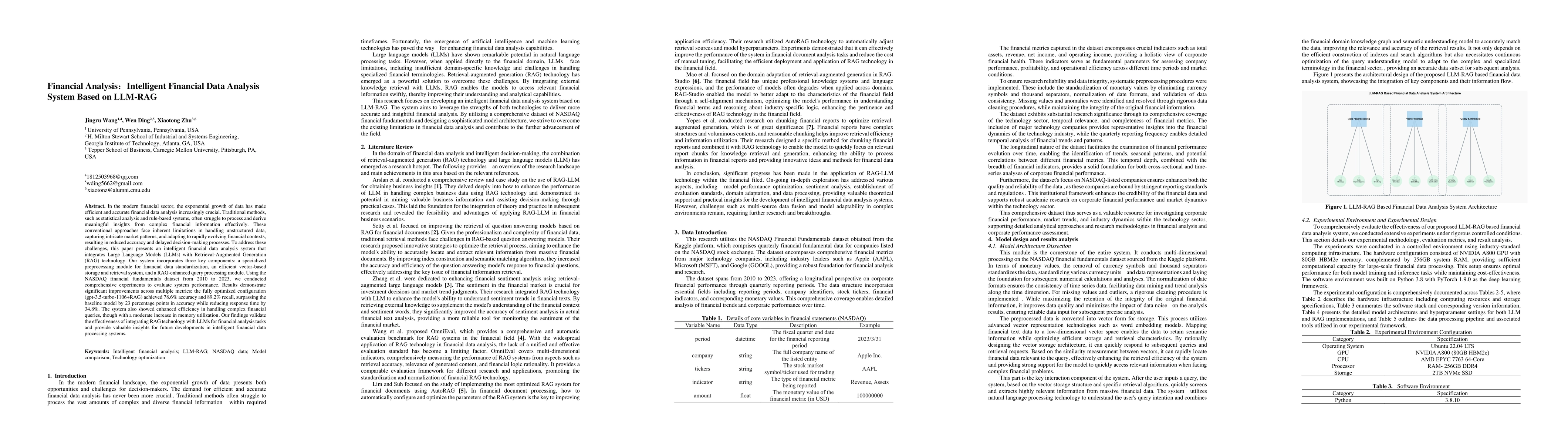

this paper presents an intelligent financial data analysis system that

integrates Large Language Models (LLMs) with Retrieval-Augmented Generation

(RAG) technology. Our system incorporates three key components: a specialized

preprocessing module for financial data standardization, an efficient

vector-based storage and retrieval system, and a RAG-enhanced query processing

module. Using the NASDAQ financial fundamentals dataset from 2010 to 2023, we

conducted comprehensive experiments to evaluate system performance. Results

demonstrate significant improvements across multiple metrics: the fully

optimized configuration (gpt-3.5-turbo-1106+RAG) achieved 78.6% accuracy and

89.2% recall, surpassing the baseline model by 23 percentage points in accuracy

while reducing response time by 34.8%. The system also showed enhanced

efficiency in handling complex financial queries, though with a moderate

increase in memory utilization. Our findings validate the effectiveness of

integrating RAG technology with LLMs for financial analysis tasks and provide

valuable insights for future developments in intelligent financial data

processing systems.

Discussion 0