01

MethodologyHow they did it

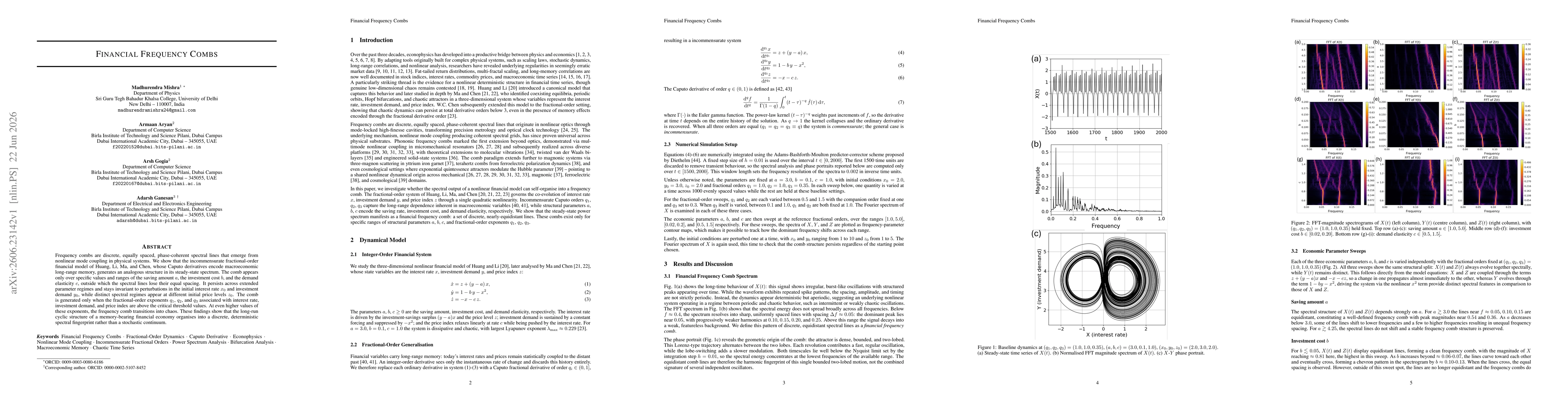

The study analyzes an incommensurate Caputo fractional-order generalization of the Huang–Li–Ma–Chen financial model, introducing fractional exponents q1, q2, q3 for the interestrate, investment demand, and price index. It investigates steady-state spectral properties by examining how discrete, nearly equidistant spectral lines (a financial frequency comb) emerge only for specific ranges of structural parameters a, b, c and fractional orders, and how these lines persist or transition to chaos as parameters vary. The approach combines fractional dynamics, spectral (power spectrum) analysis, and bifurcation theory to identify parameter regimes that produce a comb vs chaotic behavior.

Discussion 0