Financial News-Driven LLM Reinforcement Learning for Portfolio Management

Publication

Metrics

AI Quick Summary

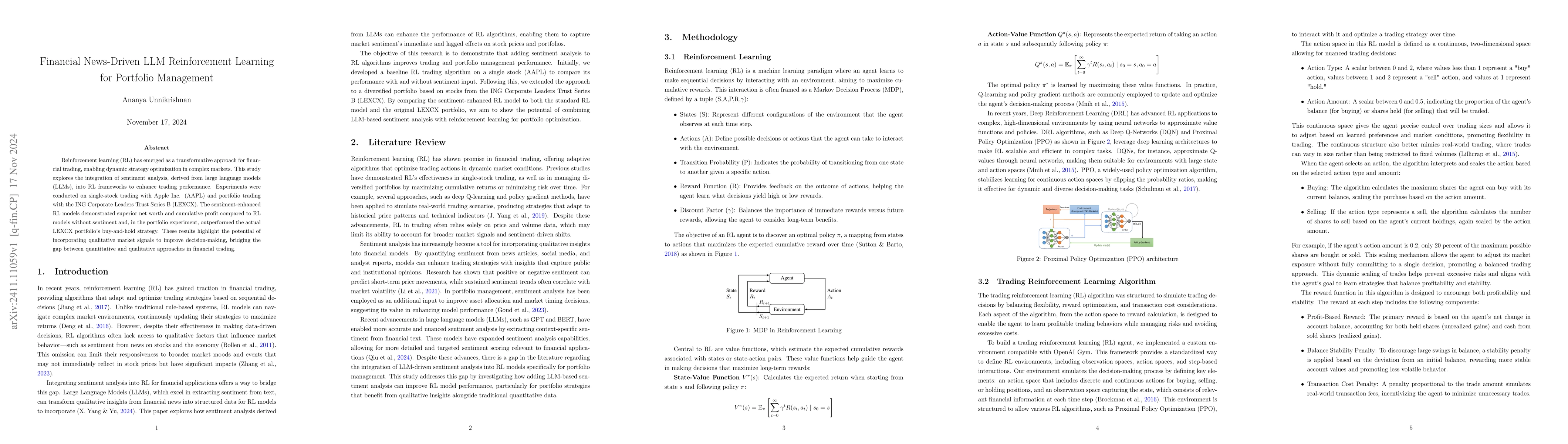

This study integrates sentiment analysis from large language models into reinforcement learning frameworks to enhance financial trading performance, showing improved outcomes in both single-stock and portfolio trading compared to traditional RL models and actual portfolio strategies. The results suggest qualitative market signals can augment quantitative trading methods.

Paper Preview

Abstract

Reinforcement learning (RL) has emerged as a transformative approach for financial trading, enabling dynamic strategy optimization in complex markets. This study explores the integration of sentiment analysis, derived from large language models (LLMs), into RL frameworks to enhance trading performance. Experiments were conducted on single-stock trading with Apple Inc. (AAPL) and portfolio trading with the ING Corporate Leaders Trust Series B (LEXCX). The sentiment-enhanced RL models demonstrated superior net worth and cumulative profit compared to RL models without sentiment and, in the portfolio experiment, outperformed the actual LEXCX portfolio's buy-and-hold strategy. These results highlight the potential of incorporating qualitative market signals to improve decision-making, bridging the gap between quantitative and qualitative approaches in financial trading.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0