01

MethodologyHow they did it

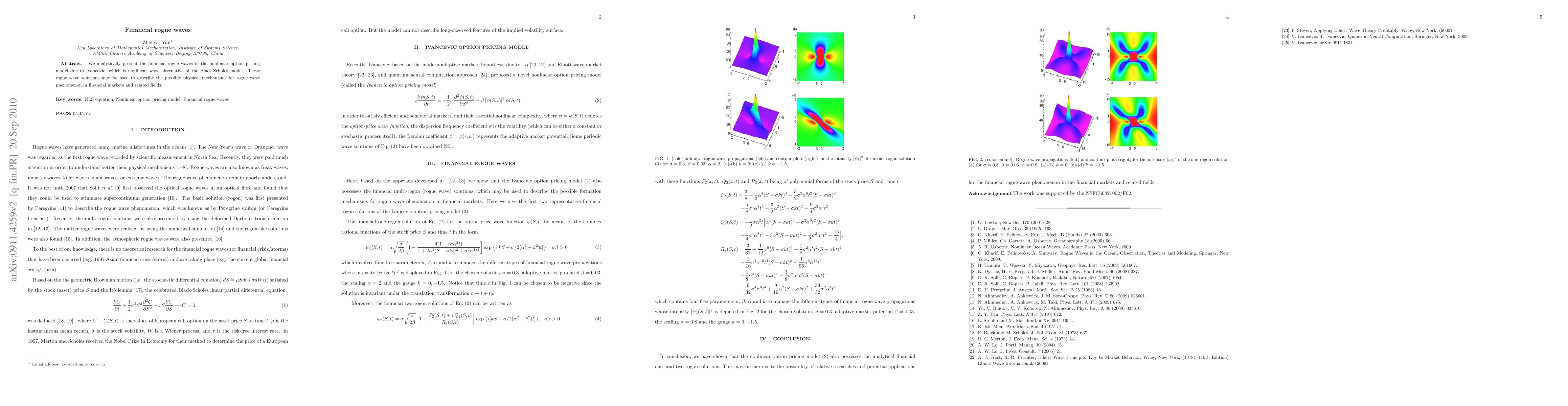

The research proposes a nonlinear option pricing model (Ivancevic option pricing model) based on the modern adaptive market hypothesis, Elliott wave market theory, and quantum neural computation approach to describe financial markets' nonlinear complexity.

Discussion 0