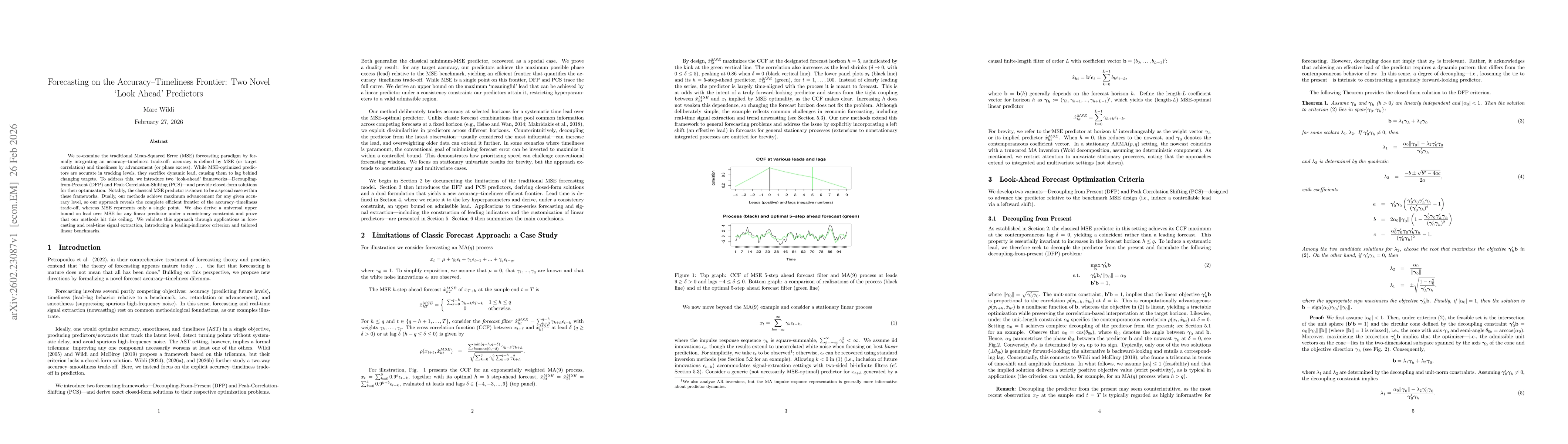

We re-examine the traditional Mean-Squared Error (MSE) forecasting paradigm by formally integrating an accuracy-timeliness trade-off: accuracy is defined by MSE (or target correlation) and timeliness by advancement (or phase excess). While MSE-optimized predictors are accurate in tracking levels, they sacrifice dynamic lead, causing them to lag behind changing targets. To address this, we introduce two `look-ahead' frameworks--Decoupling-from-Present (DFP) and Peak-Correlation-Shifting (PCS)--and provide closed-form solutions for their optimization. Notably, the classical MSE predictor is shown to be a special case within these frameworks. Dually, our methods achieve maximum advancement for any given accuracy level, so our approach reveals the complete efficient frontier of the accuracy-timeliness trade-off, whereas MSE represents only a single point. We also derive a universal upper bound on lead over MSE for any linear predictor under a consistency constraint and prove that our methods hit this ceiling. We validate this approach through applications in forecasting and real-time signal extraction, introducing a leading-indicator criterion and tailored linear benchmarks.

Discussion 0