Publication

Metrics

AI Quick Summary

This paper discusses Fryzlewicz's (2020) WBS2.SDLL method for detecting frequent change-points in mean series, emphasizing potential model misspecification issues. It uses numerical examples like self-exciting threshold autoregression and unit root processes to illustrate confusion with frequent change-point models.

Paper Preview

Abstract

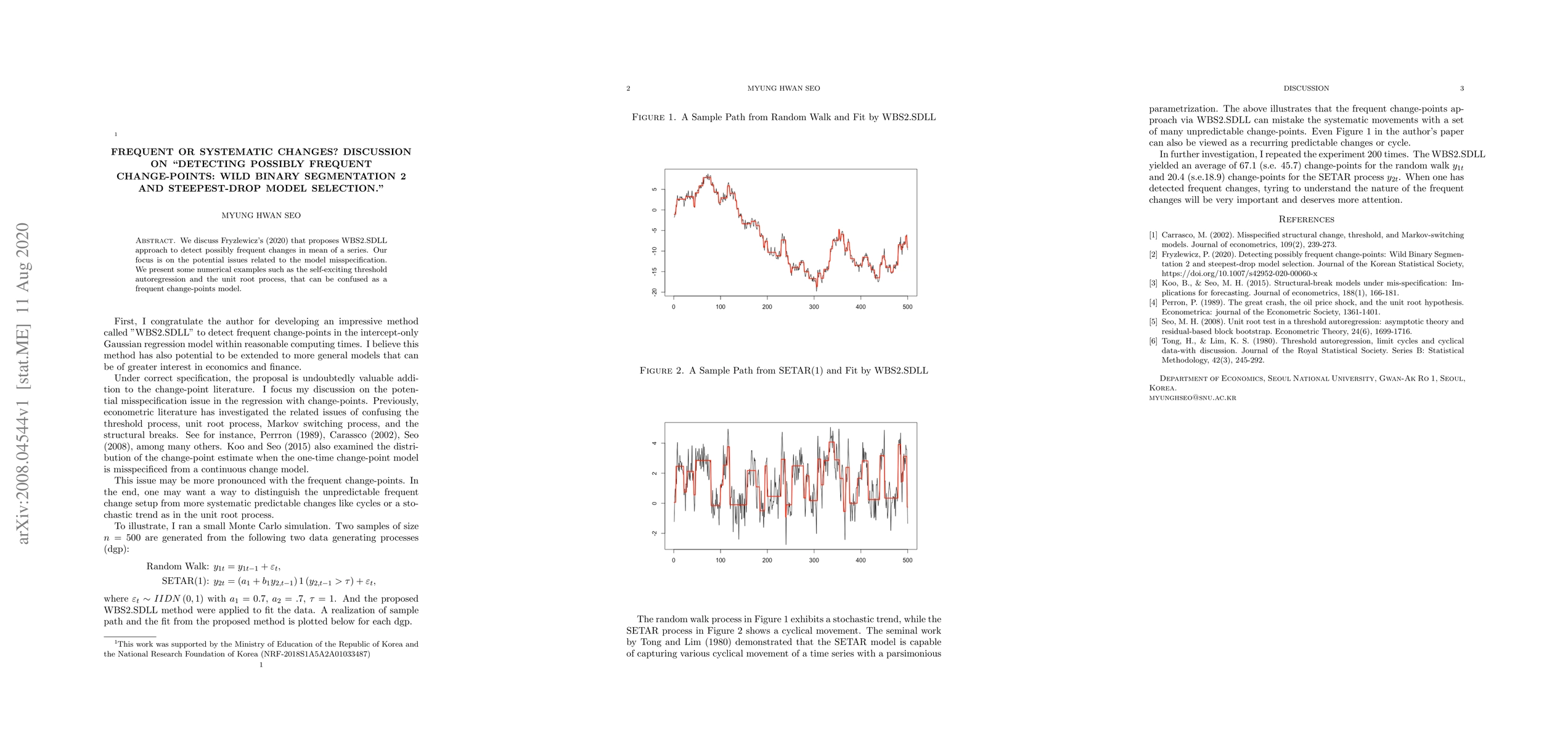

We discuss Fryzlewicz's (2020) that proposes WBS2.SDLL approach to detect possibly frequent changes in mean of a series. Our focus is on the potential issues related to the model misspecification. We present some numerical examples such as the self-exciting threshold autoregression and the unit root process, that can be confused as a frequent change-points model.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0