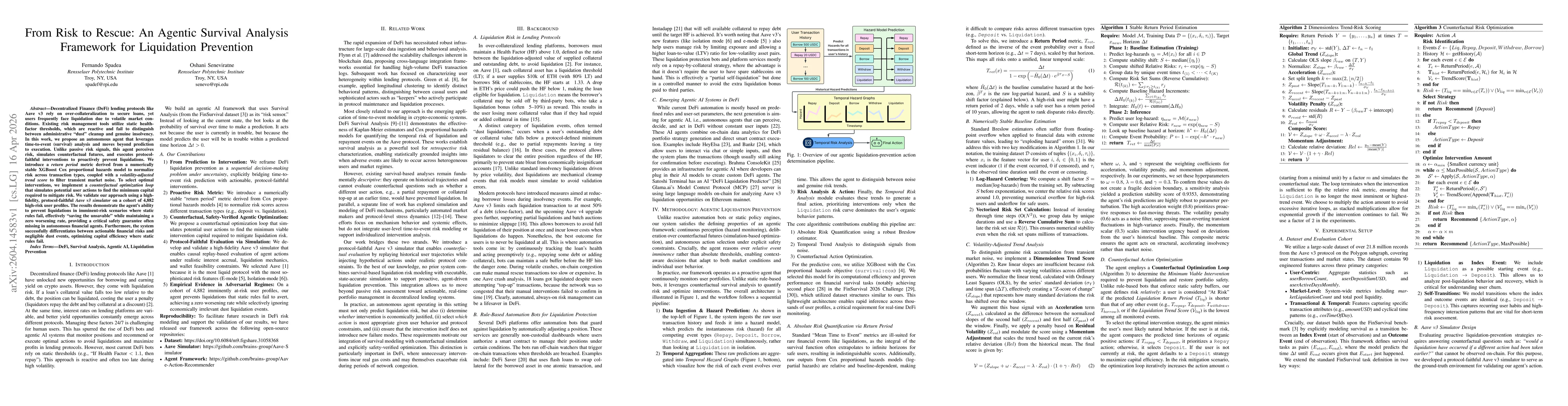

Decentralized Finance (DeFi) lending protocols like Aave v3 rely on over-collateralization to secure loans, yet users frequently face liquidation due to volatile market conditions. Existing risk management tools utilize static health-factor thresholds, which are reactive and fail to distinguish between administrative "dust" cleanup and genuine insolvency. In this work, we propose an autonomous agent that leverages time-to-event (survival) analysis and moves beyond prediction to execution. Unlike passive risk signals, this agent perceives risk, simulates counterfactual futures, and executes protocol-faithful interventions to proactively prevent liquidations. We introduce a return period metric derived from a numerically stable XGBoost Cox proportional hazards model to normalize risk across transaction types, coupled with a volatility-adjusted trend score to filter transient market noise. To select optimal interventions, we implement a counterfactual optimization loop that simulates potential user actions to find the minimum capital required to mitigate risk. We validate our approach using a high-fidelity, protocol-faithful Aave v3 simulator on a cohort of 4,882 high-risk user profiles. The results demonstrate the agent's ability to prevent liquidations in imminent-risk scenarios where static rules fail, effectively "saving the unsavable" while maintaining a zero worsening rate, providing a critical safety guarantee often missing in autonomous financial agents. Furthermore, the system successfully differentiates between actionable financial risks and negligible dust events, optimizing capital efficiency where static rules fail.

Discussion 0