Generalized exponential basis for efficient solving of homogeneous diffusion free boundary problems: Russian option pricing

Publication

Metrics

AI Quick Summary

A new method for solving homogeneous diffusion free boundary problems using a generalized exponential basis is presented, with applications to Russian option pricing and comparison to existing literature results.

Paper Preview

Abstract

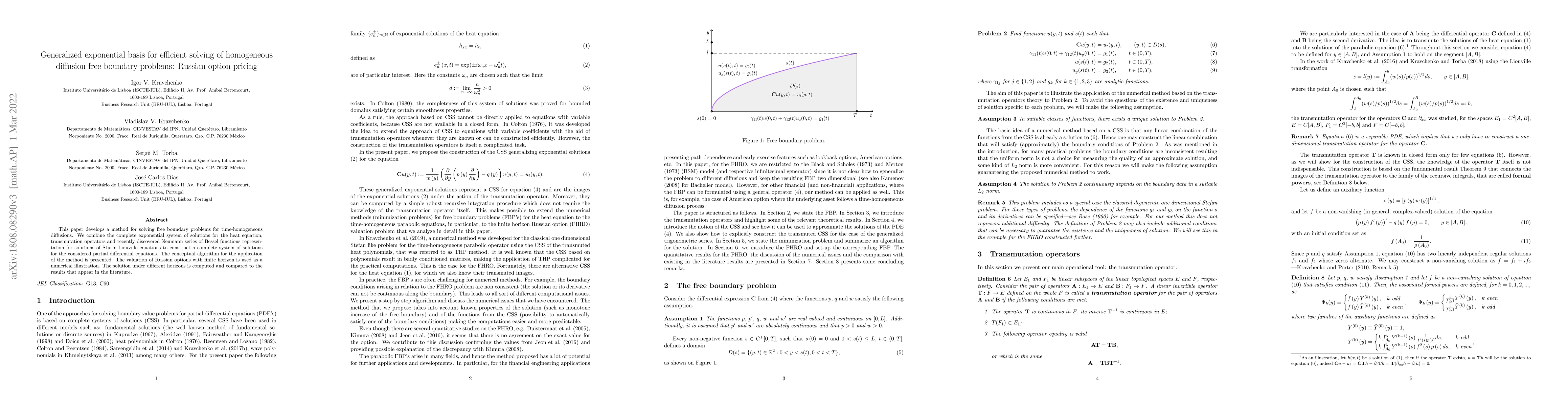

This paper develops a method for solving free boundary problems for time-homogeneous diffusions. We combine the complete exponential system of solutions for the heat equation, transmutation operators and recently discovered Neumann series of Bessel functions representation for solutions of Sturm-Liouville equations to construct a complete system of solutions for the considered partial differential equations. The conceptual algorithm for the application of the method is presented. The valuation of Russian options with finite horizon is used as a numerical illustration. The solution under different horizons is computed and compared to the results that appear in the literature.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0