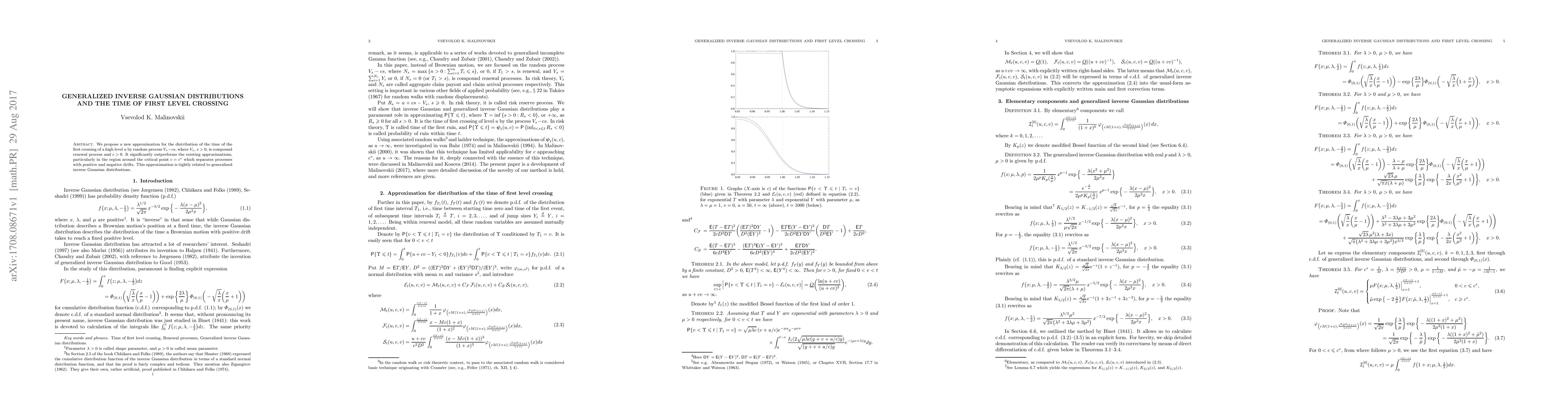

Generalized inverse Gaussian distributions and the time of first level crossing

Publication

Metrics

AI Quick Summary

Summary: This paper proposes a new approximation for the distribution of the first crossing time of a high level by a compound renewal process, significantly improving existing methods, especially near the critical drift point. The approximation leverages generalized inverse Gaussian distributions for enhanced accuracy.

Paper Preview

Abstract

We propose a new approximation for the distribution of the time of the first crossing of a high level $u$ by random process $\homV{s}-cs$, where $\homV{s}$, $s>0$, is compound renewal process and $c>0$. It significantly outperforms the existing approximations, particularly in the region around the critical point $c=\cS$ which separates processes with positive and negative drifts. This approximation is tightly related to generalized inverse Gaussian distributions.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0