Publication

Metrics

AI Quick Summary

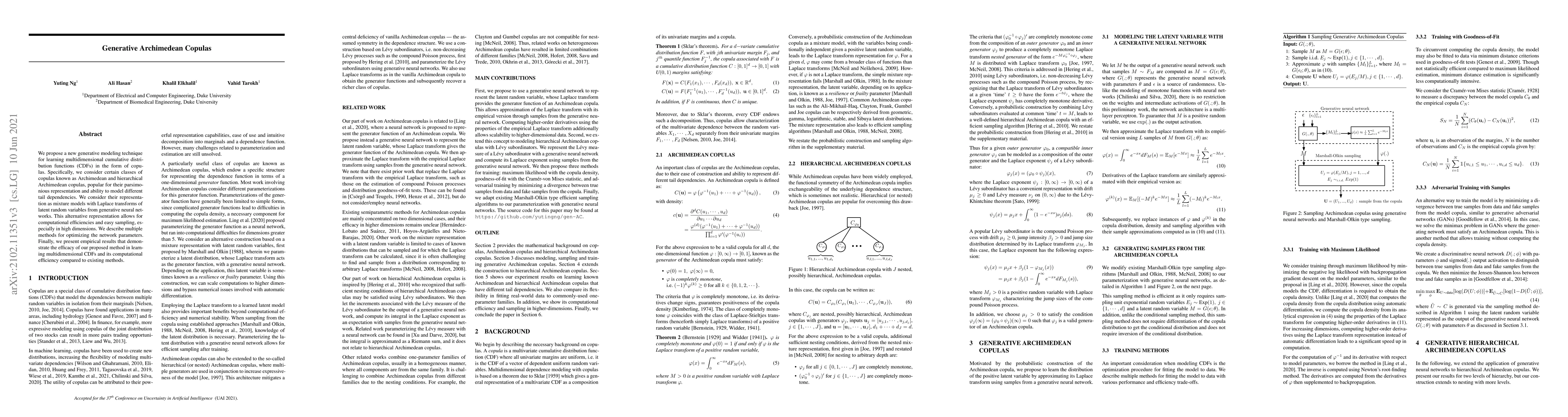

This paper introduces a novel generative modeling technique for learning Archimedean copulas, represented as mixture models with neural networks, to efficiently model multidimensional cumulative distribution functions and tail dependencies. The proposed method demonstrates superior computational efficiency and effectiveness over existing methods, as shown through empirical results.

Paper Preview

Abstract

We propose a new generative modeling technique for learning multidimensional cumulative distribution functions (CDFs) in the form of copulas. Specifically, we consider certain classes of copulas known as Archimedean and hierarchical Archimedean copulas, popular for their parsimonious representation and ability to model different tail dependencies. We consider their representation as mixture models with Laplace transforms of latent random variables from generative neural networks. This alternative representation allows for computational efficiencies and easy sampling, especially in high dimensions. We describe multiple methods for optimizing the network parameters. Finally, we present empirical results that demonstrate the efficacy of our proposed method in learning multidimensional CDFs and its computational efficiency compared to existing methods.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0