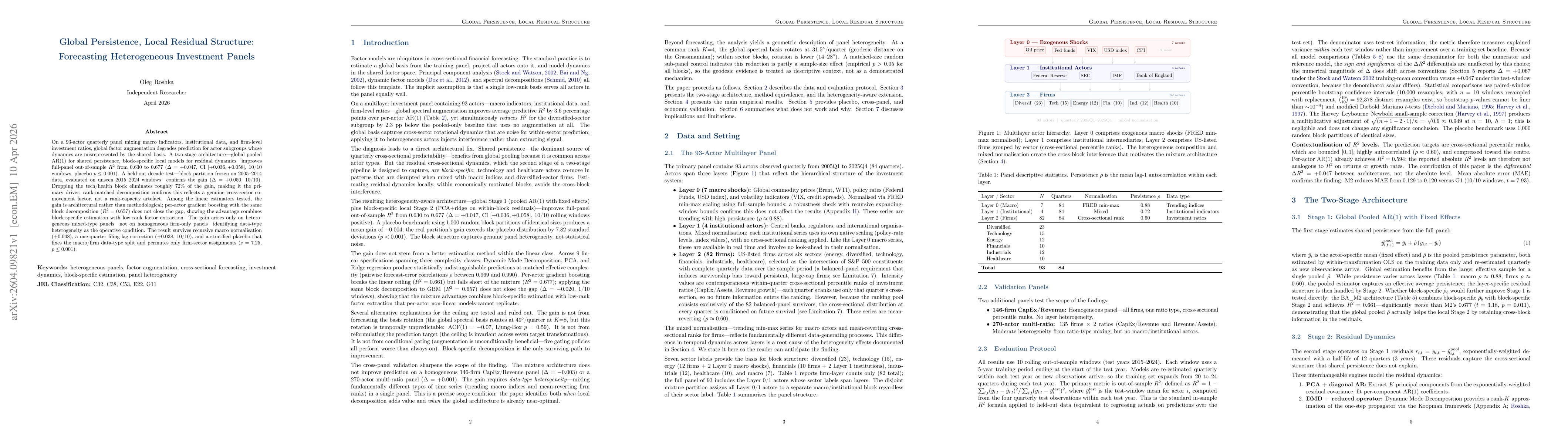

On a 93-actor quarterly panel mixing macro indicators, institutional data, and firm-level investment ratios, global factor augmentation degrades prediction for actor subgroups whose dynamics are misrepresented by the shared basis. A two-stage architecture -- global pooled AR(1) for shared persistence, block-specific local models for residual dynamics -- improves full-panel out-of-sample $R^2$ from 0.630 to 0.677 ($Δ= +0.047$, CI $[+0.036, +0.058]$, 10/10 windows, placebo $p \leq 0.001$). A held-out decade test -- block partition frozen on 2005--2014 data, evaluated on unseen 2015--2024 windows -- confirms the gain ($Δ= +0.050$, 10/10). Dropping the tech/health block eliminates roughly 72\% of the gain, making it the primary driver; rank-matched decomposition confirms this reflects a genuine cross-sector co-movement factor, not a rank-capacity artefact. Among the linear estimators tested, the gain is architectural rather than methodological; per-actor gradient boosting with the same block decomposition ($R^2 = 0.657$) does not close the gap, showing the advantage combines block-specific estimation with low-rank factor extraction. The gain arises only on heterogeneous mixed-type panels -- not on homogeneous firm-only panels -- identifying data-type heterogeneity as the operative condition. The result survives recursive macro normalisation ($+0.048$), a one-quarter filing-lag correction ($+0.038$, 10/10), and a stratified placebo that fixes the macro/firm data-type split and permutes only firm-sector assignments ($z = 7.25$, $p \leq 0.001$).

Discussion 0