Green bubbles: a four-stage paradigm for detection and propagation

Publication

Metrics

AI Quick Summary

This paper introduces a four-stage paradigm to detect and analyze "green bubbles" in the renewable energy sector, employing Statistical Process Control and econometric models. It emphasizes the necessity of these market dynamics for a sustainable transition, despite potential financial risks.

Paper Preview

Abstract

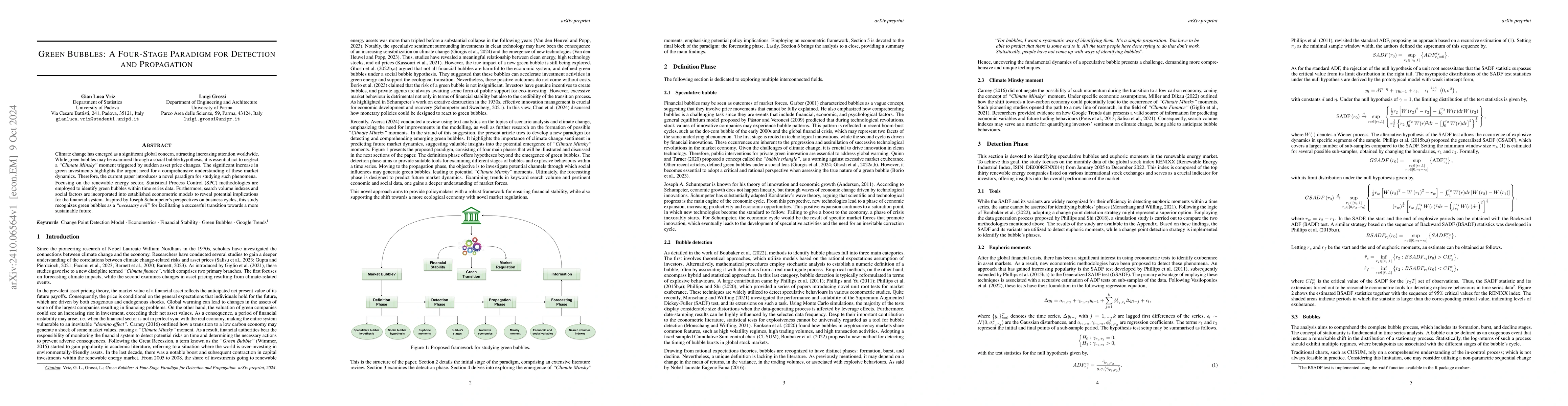

Climate change has emerged as a significant global concern, attracting increasing attention worldwide. While green bubbles may be examined through a social bubble hypothesis, it is essential not to neglect a Climate Minsky moment triggered by sudden asset price changes. The significant increase in green investments highlights the urgent need for a comprehensive understanding of these market dynamics. Therefore, the current paper introduces a novel paradigm for studying such phenomena. Focusing on the renewable energy sector, Statistical Process Control (SPC) methodologies are employed to identify green bubbles within time series data. Furthermore, search volume indexes and social factors are incorporated into established econometric models to reveal potential implications for the financial system. Inspired by Joseph Schumpeter's perspectives on business cycles, this study recognizes green bubbles as a necessary evil for facilitating a successful transition towards a more sustainable future.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0