Long-term time series forecasting is critical in domains such as finance,

economics, and energy, where accurate and reliable predictions over extended

horizons drive strategic decision-making. Despite the progress in machine

learning-based models, the impact of temporal noise in extended lookback

windows remains underexplored, often degrading model performance and

computational efficiency. In this paper, we propose a novel framework that

addresses these challenges by integrating the Discrete Wavelet Transform (DWT)

and Discrete Cosine Transform (DCT) to perform noise reduction and extract

robust long-term features. These transformations enable the separation of

meaningful temporal patterns from noise in both the time and frequency domains.

To complement this, we introduce a lightweight low-rank linear prediction layer

that not only reduces the influence of residual noise but also improves memory

efficiency. Our approach demonstrates competitive robustness to noisy input,

significantly reduces computational complexity, and achieves competitive or

state-of-the-art forecasting performance across diverse benchmark datasets.

Extensive experiments reveal that the proposed framework is particularly

effective in scenarios with high noise levels or irregular patterns, making it

well suited for real-world forecasting tasks. The code is available in

https://github.com/forgee-master/HADL.

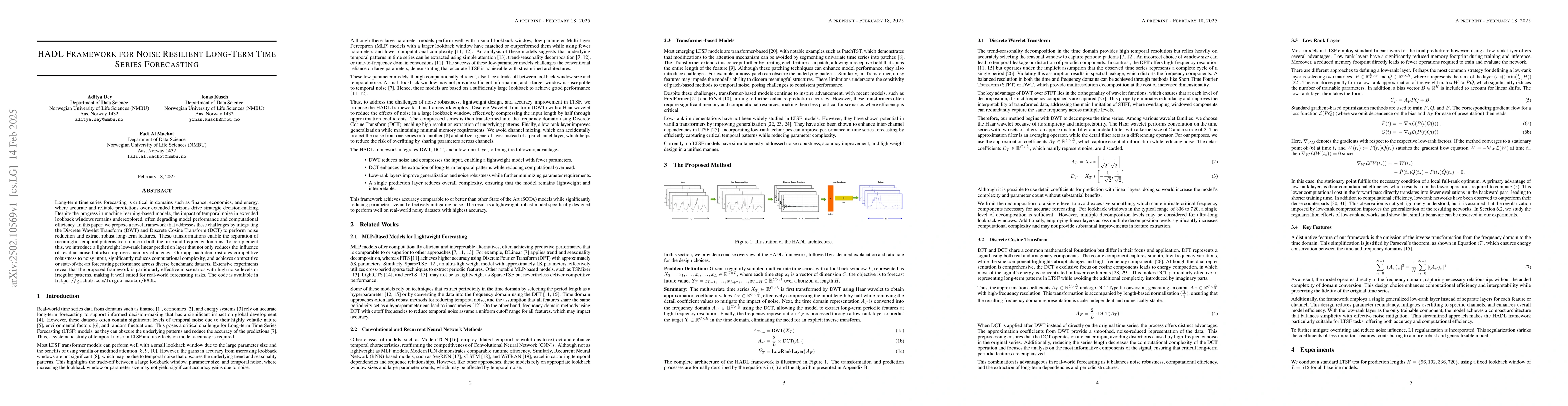

Discussion 0