Heterogeneous Graph Pre-training Based Model for Secure and Efficient Prediction of Default Risk Propagation among Bond Issuers

Publication

Metrics

AI Quick Summary

This paper proposes a two-stage model for predicting default risk among bond issuers using a heterogeneous graph pre-training approach. The first stage employs Masked Autoencoders for Heterogeneous Graph to pre-train on a large enterprise knowledge graph, and the second stage uses a classifier that combines pre-trained features with task-specific data, achieving superior performance compared to existing methods.

Paper Preview

Abstract

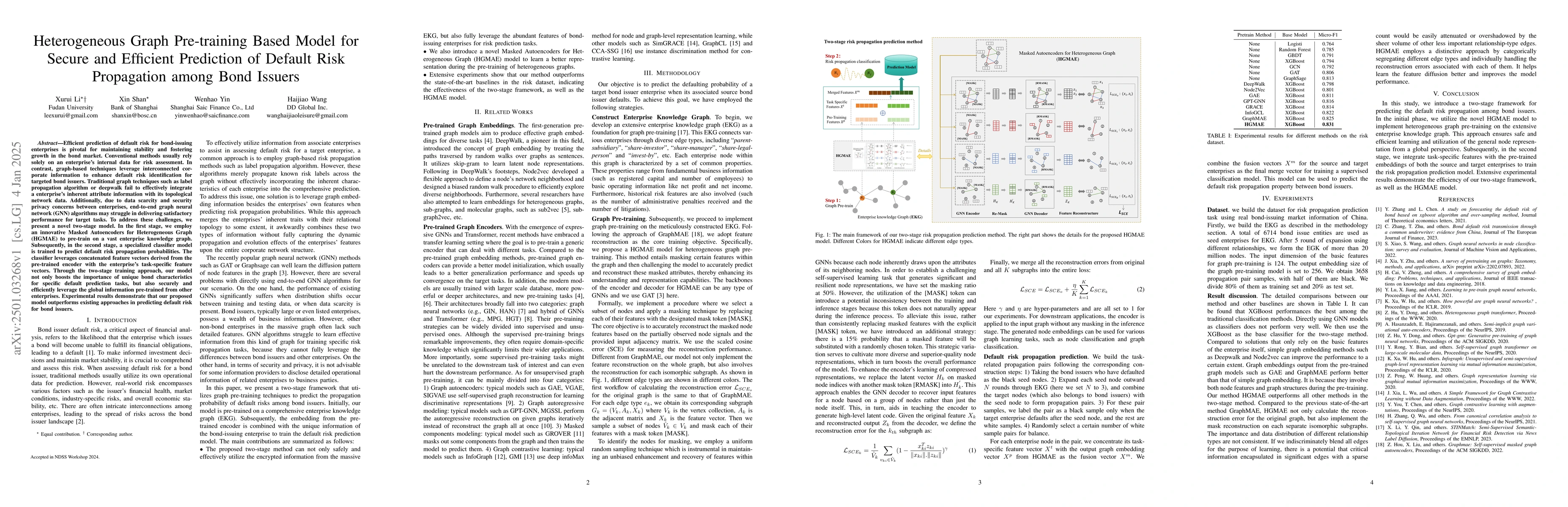

Efficient prediction of default risk for bond-issuing enterprises is pivotal for maintaining stability and fostering growth in the bond market. Conventional methods usually rely solely on an enterprise's internal data for risk assessment. In contrast, graph-based techniques leverage interconnected corporate information to enhance default risk identification for targeted bond issuers. Traditional graph techniques such as label propagation algorithm or deepwalk fail to effectively integrate a enterprise's inherent attribute information with its topological network data. Additionally, due to data scarcity and security privacy concerns between enterprises, end-to-end graph neural network (GNN) algorithms may struggle in delivering satisfactory performance for target tasks. To address these challenges, we present a novel two-stage model. In the first stage, we employ an innovative Masked Autoencoders for Heterogeneous Graph (HGMAE) to pre-train on a vast enterprise knowledge graph. Subsequently, in the second stage, a specialized classifier model is trained to predict default risk propagation probabilities. The classifier leverages concatenated feature vectors derived from the pre-trained encoder with the enterprise's task-specific feature vectors. Through the two-stage training approach, our model not only boosts the importance of unique bond characteristics for specific default prediction tasks, but also securely and efficiently leverage the global information pre-trained from other enterprises. Experimental results demonstrate that our proposed model outperforms existing approaches in predicting default risk for bond issuers.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Authors

PDF Preview

Related Papers

No references found for this paper.

Discussion 0