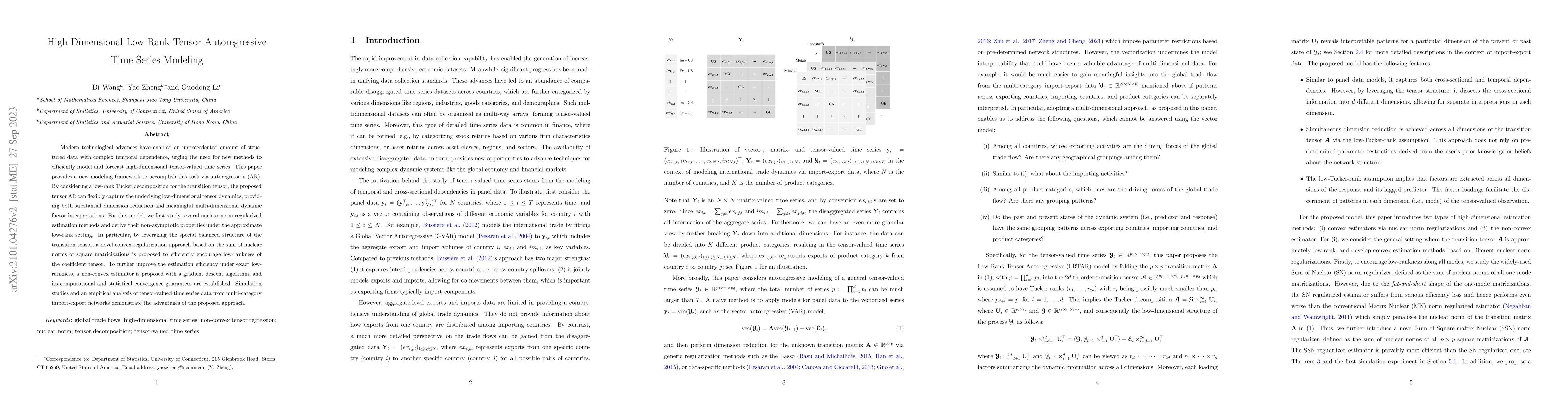

High-Dimensional Low-Rank Tensor Autoregressive Time Series Modeling

Publication

Metrics

AI Quick Summary

This paper introduces a novel high-dimensional low-rank tensor autoregressive (AR) model for forecasting complex time series data, leveraging a low-rank Tucker decomposition to capture underlying dynamics. The proposed model employs nuclear-norm and gradient descent-based regularization techniques to ensure efficient estimation and computational convergence, validated through simulations and real-world data analysis.

Paper Preview

Abstract

Modern technological advances have enabled an unprecedented amount of structured data with complex temporal dependence, urging the need for new methods to efficiently model and forecast high-dimensional tensor-valued time series. This paper provides a new modeling framework to accomplish this task via autoregression (AR). By considering a low-rank Tucker decomposition for the transition tensor, the proposed tensor AR can flexibly capture the underlying low-dimensional tensor dynamics, providing both substantial dimension reduction and meaningful multi-dimensional dynamic factor interpretations. For this model, we first study several nuclear-norm-regularized estimation methods and derive their non-asymptotic properties under the approximate low-rank setting. In particular, by leveraging the special balanced structure of the transition tensor, a novel convex regularization approach based on the sum of nuclear norms of square matricizations is proposed to efficiently encourage low-rankness of the coefficient tensor. To further improve the estimation efficiency under exact low-rankness, a non-convex estimator is proposed with a gradient descent algorithm, and its computational and statistical convergence guarantees are established. Simulation studies and an empirical analysis of tensor-valued time series data from multi-category import-export networks demonstrate the advantages of the proposed approach.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0