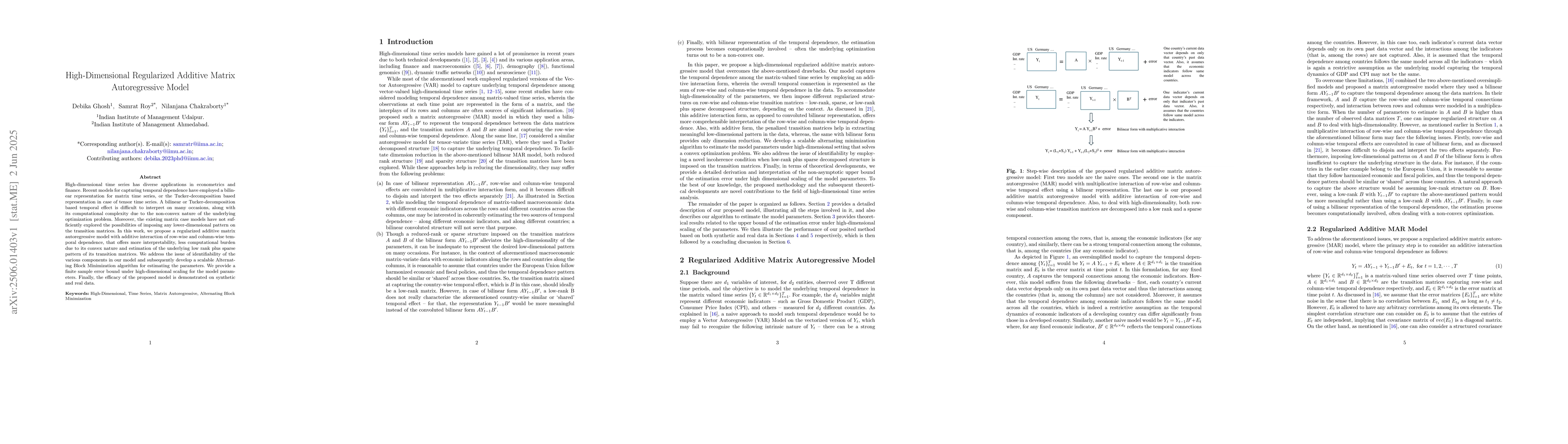

High-dimensional time series has diverse applications in econometrics and

finance. Recent models for capturing temporal dependence have employed a

bilinear representation for matrix time series, or the Tucker-decomposition

based representation in case of tensor time series. A bilinear or

Tucker-decomposition based temporal effect is difficult to interpret on many

occasions, along with its computational complexity due to the non-convex nature

of the underlying optimization problem. Moreover, the existing matrix case

models have not sufficiently explored the possibilities of imposing any

lower-dimensional pattern on the transition matrices. In this work, we propose

a regularized additive matrix autoregressive model with additive interaction of

row-wise and column-wise temporal dependence, that offers more

interpretability, less computational burden due to its convex nature and

estimation of the underlying low rank plus sparse pattern of its transition

matrices. We address the issue of identifiability of the various components in

our model and subsequently develop a scalable Alternating Block Minimization

algorithm for estimating the parameters. We provide a finite sample error bound

under high-dimensional scaling for the model parameters. Finally, the efficacy

of the proposed model is demonstrated on synthetic and real data.

Discussion 0