High Probability and Risk-Averse Guarantees for a Stochastic Accelerated Primal-Dual Method

Publication

Metrics

AI Quick Summary

This paper investigates the stochastic accelerated primal-dual algorithm (SAPD) for solving stochastic strongly-convex-strongly-concave saddle point problems, providing high probability convergence guarantees and a tight analysis of its limiting covariance matrix. It also introduces risk-averse convergence metrics to characterize the trade-offs between bias and risk in approximate solutions.

Paper Preview

Abstract

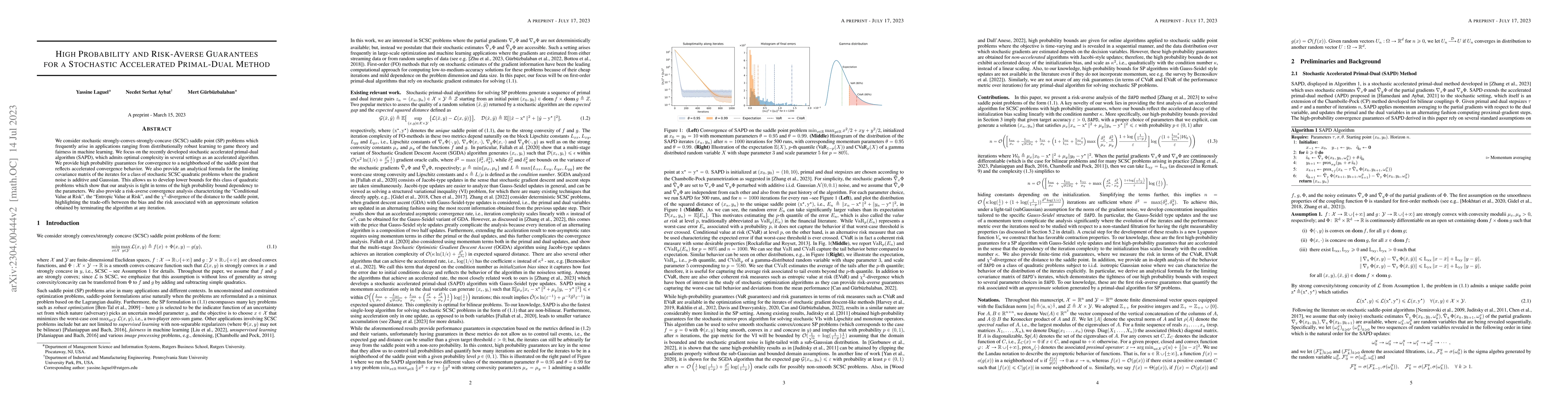

We consider stochastic strongly-convex-strongly-concave (SCSC) saddle point (SP) problems which frequently arise in applications ranging from distributionally robust learning to game theory and fairness in machine learning. We focus on the recently developed stochastic accelerated primal-dual algorithm (SAPD), which admits optimal complexity in several settings as an accelerated algorithm. We provide high probability guarantees for convergence to a neighborhood of the saddle point that reflects accelerated convergence behavior. We also provide an analytical formula for the limiting covariance matrix of the iterates for a class of stochastic SCSC quadratic problems where the gradient noise is additive and Gaussian. This allows us to develop lower bounds for this class of quadratic problems which show that our analysis is tight in terms of the high probability bound dependency to the parameters. We also provide a risk-averse convergence analysis characterizing the ``Conditional Value at Risk'', the ``Entropic Value at Risk'', and the $\chi^2$-divergence of the distance to the saddle point, highlighting the trade-offs between the bias and the risk associated with an approximate solution obtained by terminating the algorithm at any iteration.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0