Publication

Metrics

AI Quick Summary

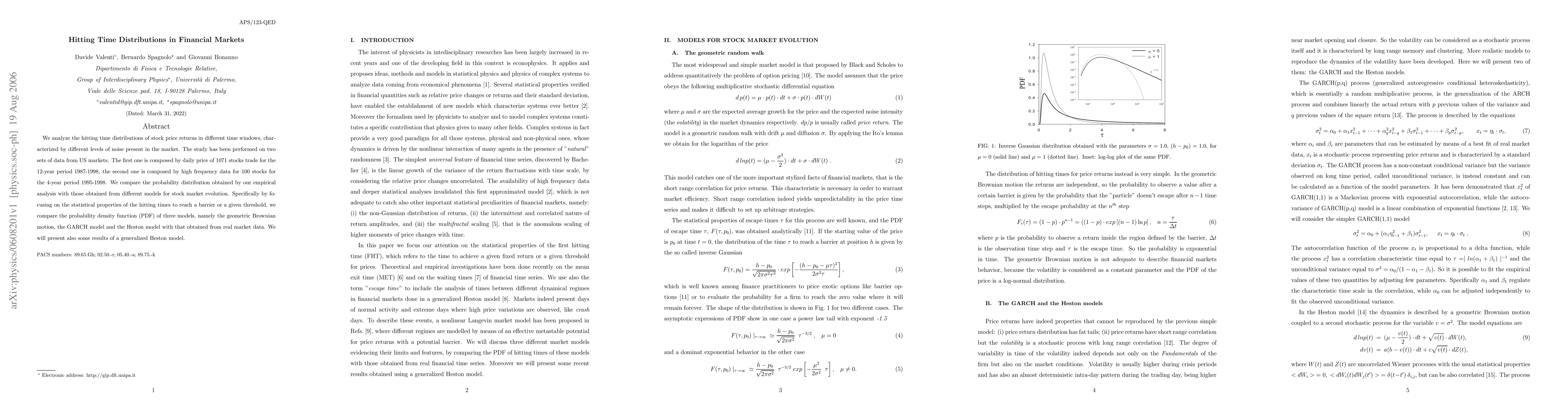

This research examines stock price return hitting time distributions across various timeframes in US markets, using both daily data (1987-1998) and high-frequency data (1995-1998). It contrasts empirical PDFs with those from geometric Brownian motion, GARCH, and Heston models, also presenting results from a generalized Heston model.

Paper Preview

Abstract

We analyze the hitting time distributions of stock price returns in different time windows, characterized by different levels of noise present in the market. The study has been performed on two sets of data from US markets. The first one is composed by daily price of 1071 stocks trade for the 12-year period 1987-1998, the second one is composed by high frequency data for 100 stocks for the 4-year period 1995-1998. We compare the probability distribution obtained by our empirical analysis with those obtained from different models for stock market evolution. Specifically by focusing on the statistical properties of the hitting times to reach a barrier or a given threshold, we compare the probability density function (PDF) of three models, namely the geometric Brownian motion, the GARCH model and the Heston model with that obtained from real market data. We will present also some results of a generalized Heston model.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0