The study employs a probabilistic analysis of a reactive gambling strategy where the bet size is adjusted based on previous outcomes. The gambler doubles the bet after each win and halves it after each loss, with the probability of winning each round denoted by $ p ". KeyResults": ["The gambler survives with positive probability if and only if $ p < 1/2 $ and $ x > 2 $.", "The ruin probability is increasing in $ p $ and real-analytic, but a singular, Hölder continuous function of the initial fortune $ x $.", "The analysis shows that the process $ (M_n) $ is a submartingale and derives bounds on the ruin probability using martingale techniques."], "Significance": "This research provides critical insights into the behavior of reactive gambling strategies, highlighting the conditions under which gamblers can avoid ruin. It contributes to the understanding of stochastic processes and their applications in gambling theory, with implications for risk management and probability analysis.", "Limitations": ["The analysis focuses on a specific betting strategy with fixed adjustment rules, limiting generalizability to other betting mechanisms.", "The results are derived under the assumption of a fixed probability $ p $, which may not capture real-world variability in winning probabilities.", "The mathematical complexity may restrict practical applications in real-time gambling scenarios."], "FutureWork": ["Exploring the extension of these results to more complex betting strategies with variable adjustment rules.", "Investigating the impact of time-dependent probabilities on ruin probabilities in reactive gambling.", "Applying the findings to other stochastic processes with similar recursive structures.", "Developing computational models to simulate and validate the theoretical results in practical scenarios.", "Examining the interplay between initial fortune and long-term survival probabilities in different gambling frameworks."], "TechnicalContribution": "The paper introduces a rigorous mathematical framework to analyze the ruin probability in a reactive gambling strategy, leveraging martingale theory and properties of Hölder continuity to derive key results about the dependence of ruin probabilities on the winning probability and initial fortune.", "Novelty": "This work is novel in its combination of martingale techniques with Hölder continuity analysis to study the ruin probability in a non-standard gambling process, offering new perspectives on the interplay between betting strategies and stochastic outcomes."}

How reactive gambling can backfire: ruin probability is increasing in $p$, Hölder continuous in initial fortune

Publication

Metrics

Quick Answers

What methodology did the authors use?

The study employs a probabilistic analysis of a reactive gambling strategy where the bet size is adjusted based on previous outcomes. The gambler doubles the bet after each win and halves it after each loss, with the probability of winning each round denoted by $ p ". KeyResults": ["The gambler survives with positive probability if and only if $ p... More in Methodology →

Paper Preview

Abstract

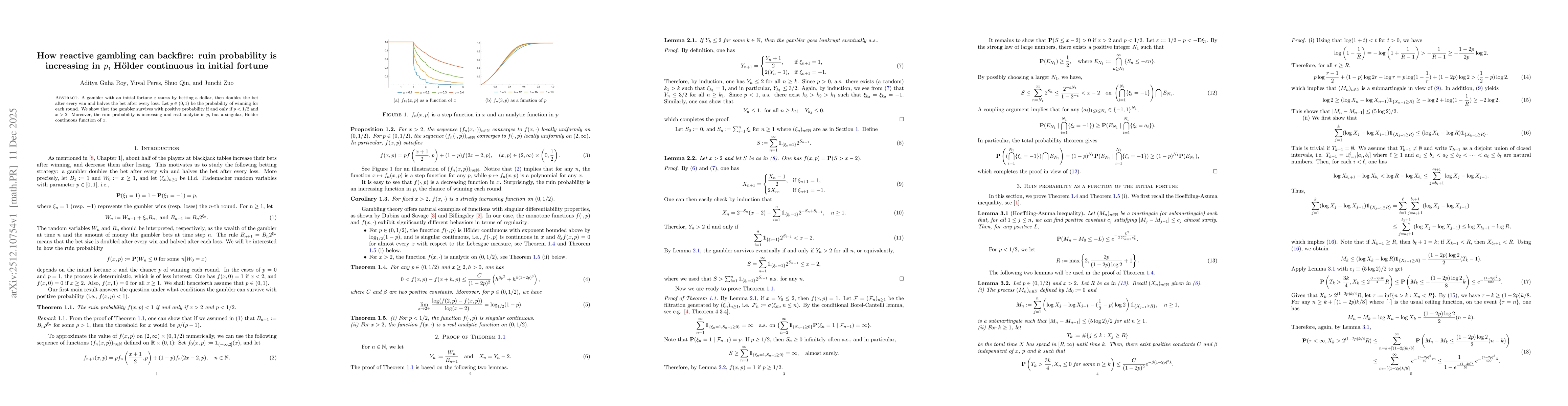

A gambler with an initial fortune $x$ starts by betting a dollar, then doubles the bet after every win and halves the bet after every loss. Let $p\in (0,1)$ be the probability of winning for each round. We show that the gambler survives with positive probability if and only if $p < 1/2$ and $x > 2$. Moreover, the ruin probability is increasing and real-analytic in $p$, but a singular, Hölder continuous function of $x$.

Key Findings, in focus

Seven facets of this paper, analysed and brought into focus by AI.

The study employs a probabilistic analysis of a reactive gambling strategy where the bet size is adjusted based on previous outcomes.

Discussion 0