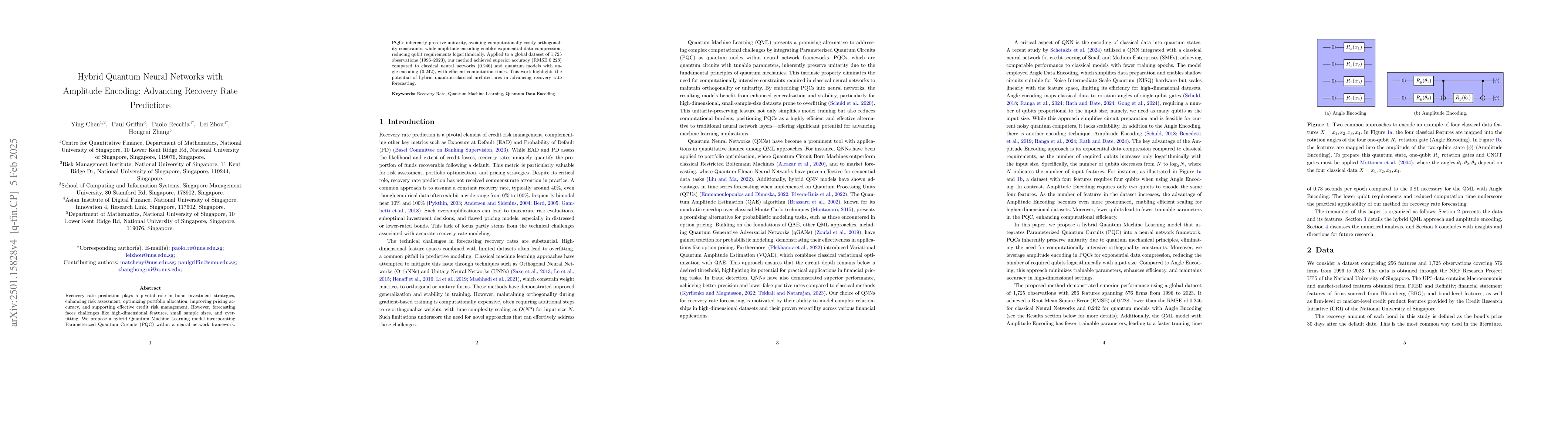

Recovery rate prediction plays a pivotal role in bond investment strategies,

enhancing risk assessment, optimizing portfolio allocation, improving pricing

accuracy, and supporting effective credit risk management. However, forecasting

faces challenges like high-dimensional features, small sample sizes, and

overfitting. We propose a hybrid Quantum Machine Learning model incorporating

Parameterized Quantum Circuits (PQC) within a neural network framework. PQCs

inherently preserve unitarity, avoiding computationally costly orthogonality

constraints, while amplitude encoding enables exponential data compression,

reducing qubit requirements logarithmically. Applied to a global dataset of

1,725 observations (1996-2023), our method achieved superior accuracy (RMSE

0.228) compared to classical neural networks (0.246) and quantum models with

angle encoding (0.242), with efficient computation times. This work highlights

the potential of hybrid quantum-classical architectures in advancing recovery

rate forecasting.

Discussion 0