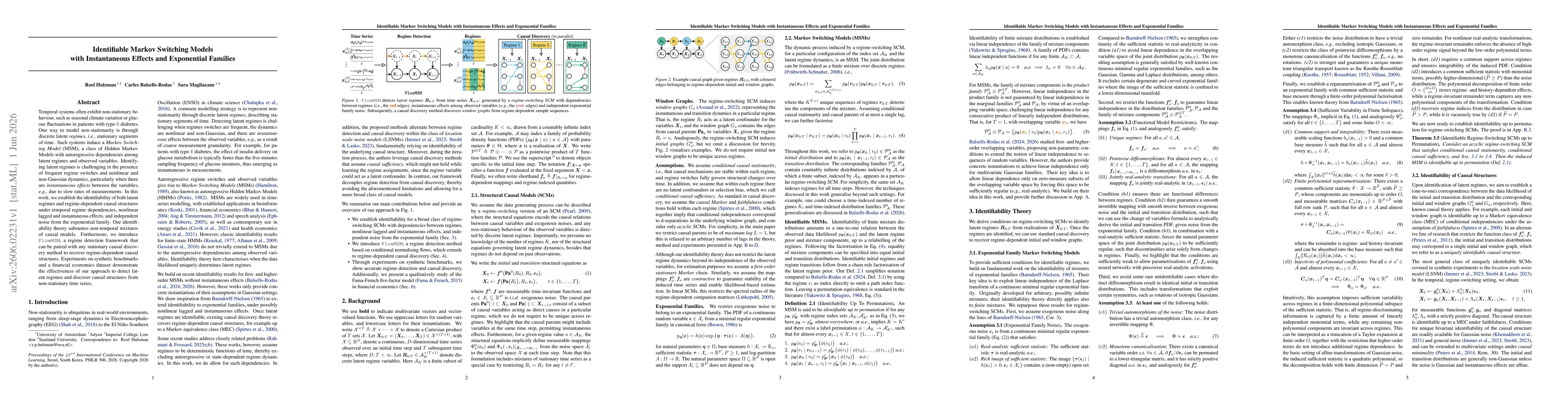

Temporal systems often exhibit non-stationary behaviour, such as seasonal climate variation or glucose fluctuations in patients with type-1 diabetes. One way to model non-stationarity is through discrete latent regimes, i.e., stationary segments of time. Such systems induce a Markov Switching Model (MSM), a class of Hidden Markov Models with autoregressive dependencies among latent regimes and observed variables. Identifying latent regimes is challenging in the presence of frequent regime switches and nonlinear and non-Gaussian dynamics, particularly when there are instantaneous effects between the variables, e.g., due to slow rates of measurements. In this work, we establish the identifiability of both latent regimes and regime-dependent causal structures under temporal regime dependencies, nonlinear lagged and instantaneous effects, and independent noise from the exponential family. Our identifiability theory subsumes non-temporal mixtures of causal models. Furthermore, we introduce FlowMSM, a regime detection framework that can be paired with any stationary causal discovery method to recover regime-dependent causal structures. Experiments on synthetic benchmarks and a financial economics dataset demonstrate the effectiveness of our approach to detect latent regimes and discover causal structures from non-stationary time series.

Discussion 0