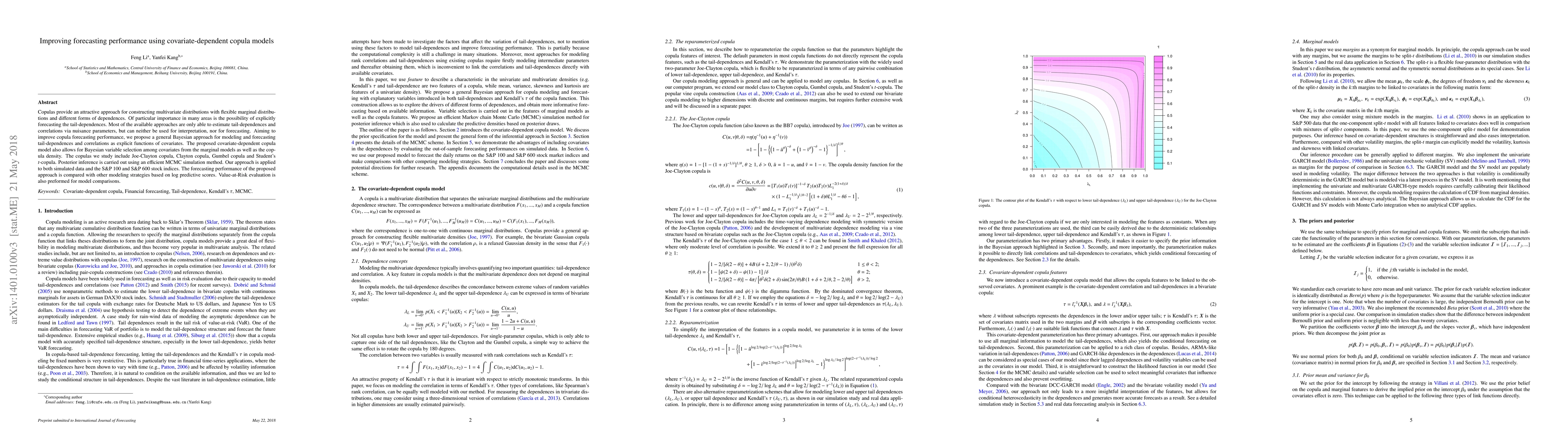

Improving forecasting performance using covariate-dependent copula models

Publication

Metrics

AI Quick Summary

This research introduces a Bayesian approach using covariate-dependent copula models to enhance forecasting performance by explicitly modeling tail-dependences and correlations as functions of covariates. The method includes variable selection and applies to various copula types, demonstrating improved log predictive scores and Value-at-Risk evaluation compared to other strategies through simulations and real stock index data analysis.

Paper Preview

Abstract

Copulas provide an attractive approach for constructing multivariate distributions with flexible marginal distributions and different forms of dependences. Of particular importance in many areas is the possibility of explicitly forecasting the tail-dependences. Most of the available approaches are only able to estimate tail-dependences and correlations via nuisance parameters, but can neither be used for interpretation, nor for forecasting. Aiming to improve copula forecasting performance, we propose a general Bayesian approach for modeling and forecasting tail-dependences and correlations as explicit functions of covariates. The proposed covariate-dependent copula model also allows for Bayesian variable selection among covariates from the marginal models as well as the copula density. The copulas we study include Joe-Clayton copula, Clayton copula, Gumbel copula and Student's \emph{t}-copula. Posterior inference is carried out using an efficient MCMC simulation method. Our approach is applied to both simulated data and the S\&P 100 and S\&P 600 stock indices. The forecasting performance of the proposed approach is compared with other modeling strategies based on log predictive scores. Value-at-Risk evaluation is also preformed for model comparisons.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0