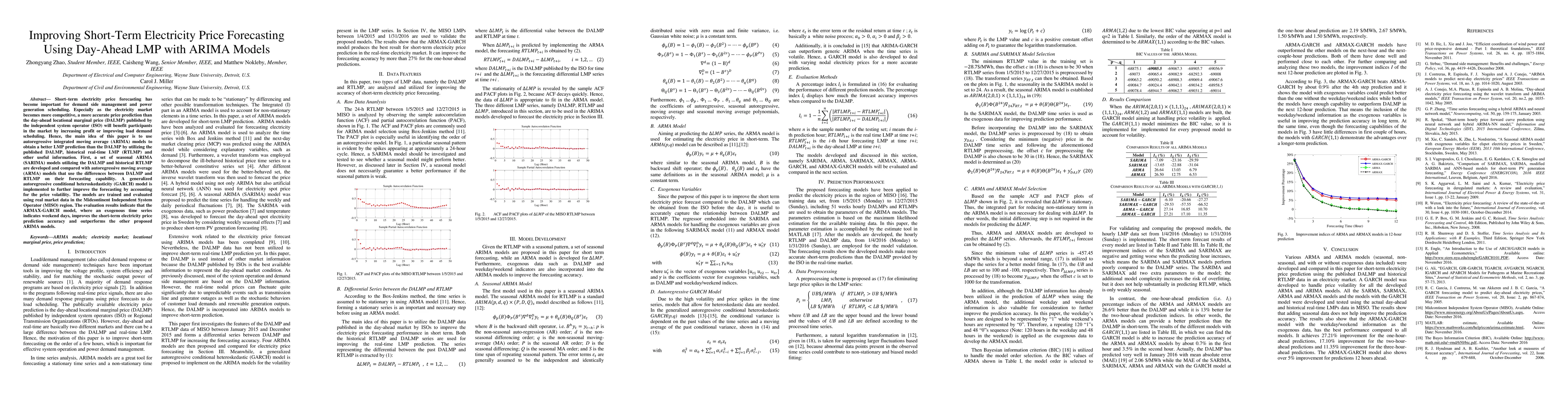

Publication

Metrics

AI Quick Summary

This paper proposes ARIMA models, including SARIMA and ARMAX-GARCH, to enhance the accuracy of short-term electricity price forecasting beyond the day-ahead locational marginal price (DALMP). The study demonstrates that the ARMAX-GARCH model, incorporating weekend indicators, outperforms traditional ARIMA models in forecasting short-term electricity prices in the MISO region.

Paper Preview

Abstract

Short-term electricity price forecasting has become important for demand side management and power generation scheduling. Especially as the electricity market becomes more competitive, a more accurate price prediction than the day-ahead locational marginal price (DALMP) published by the independent system operator (ISO) will benefit participants in the market by increasing profit or improving load demand scheduling. Hence, the main idea of this paper is to use autoregressive integrated moving average (ARIMA) models to obtain a better LMP prediction than the DALMP by utilizing the published DALMP, historical real-time LMP (RTLMP) and other useful information. First, a set of seasonal ARIMA (SARIMA) models utilizing the DALMP and historical RTLMP are developed and compared with autoregressive moving average (ARMA) models that use the differences between DALMP and RTLMP on their forecasting capability. A generalized autoregressive conditional heteroskedasticity (GARCH) model is implemented to further improve the forecasting by accounting for the price volatility. The models are trained and evaluated using real market data in the Midcontinent Independent System Operator (MISO) region. The evaluation results indicate that the ARMAX-GARCH model, where an exogenous time series indicates weekend days, improves the short-term electricity price prediction accuracy and outperforms the other proposed ARIMA models

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0