Incremental Learning of Stock Trends via Meta-Learning with Dynamic Adaptation

Publication

Metrics

AI Quick Summary

This paper proposes MetaDA, a meta-learning approach with dynamic adaptation for incremental stock trend forecasting, which leverages both recent and historical data to improve forecasting accuracy. The method dynamically selects relevant historical data to complement the latest trends, achieving state-of-the-art performance on real-world stock datasets.

Paper Preview

Abstract

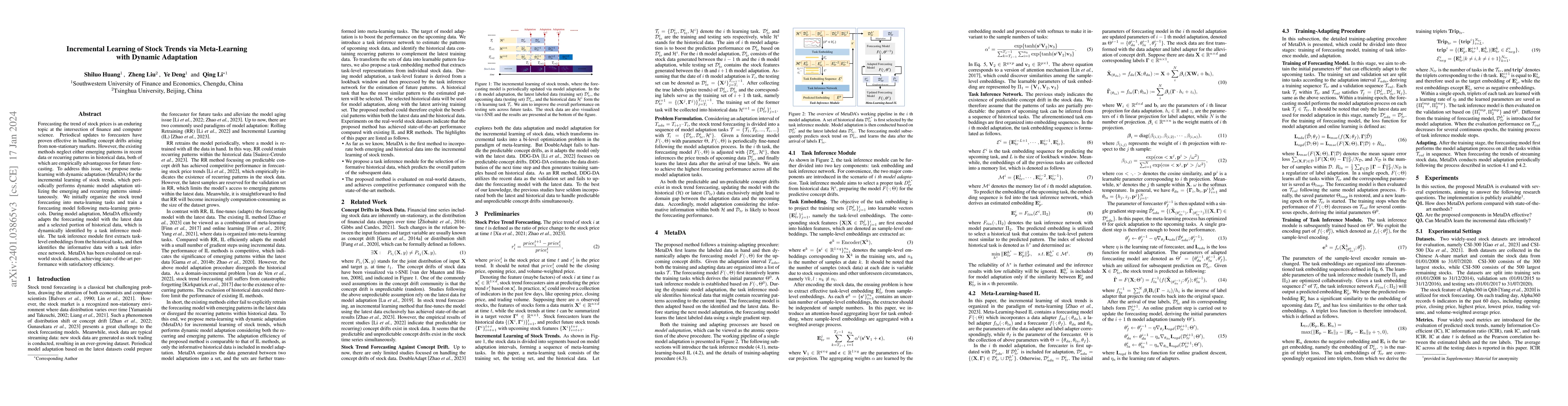

Forecasting the trend of stock prices is an enduring topic at the intersection of finance and computer science. Periodical updates to forecasters have proven effective in handling concept drifts arising from non-stationary markets. However, the existing methods neglect either emerging patterns in recent data or recurring patterns in historical data, both of which are empirically advantageous for future forecasting. To address this issue, we propose meta-learning with dynamic adaptation (MetaDA) for the incremental learning of stock trends, which periodically performs dynamic model adaptation utilizing the emerging and recurring patterns simultaneously. We initially organize the stock trend forecasting into meta-learning tasks and train a forecasting model following meta-learning protocols. During model adaptation, MetaDA efficiently adapts the forecasting model with the latest data and a selected portion of historical data, which is dynamically identified by a task inference module. The task inference module first extracts task-level embeddings from the historical tasks, and then identifies the informative data with a task inference network. MetaDA has been evaluated on real-world stock datasets, achieving state-of-the-art performance with satisfactory efficiency.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0