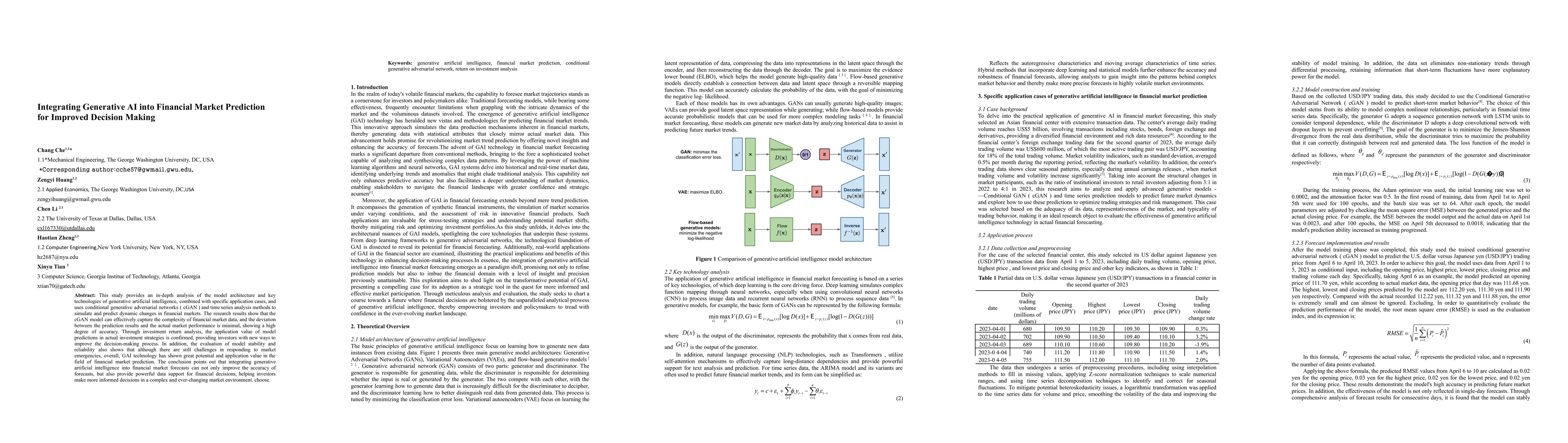

Integrating Generative AI into Financial Market Prediction for Improved Decision Making

Publication

Metrics

AI Quick Summary

This study explores the integration of generative AI, specifically conditional generative adversarial networks (cGAN), with time series analysis to predict financial market changes, demonstrating high accuracy in capturing market complexities and minimal deviation from actual performance.

Paper Preview

Abstract

This study provides an in-depth analysis of the model architecture and key technologies of generative artificial intelligence, combined with specific application cases, and uses conditional generative adversarial networks ( cGAN ) and time series analysis methods to simulate and predict dynamic changes in financial markets. The research results show that the cGAN model can effectively capture the complexity of financial market data, and the deviation between the prediction results and the actual market performance is minimal, showing a high degree of accuracy.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0