01

MethodologyHow they did it

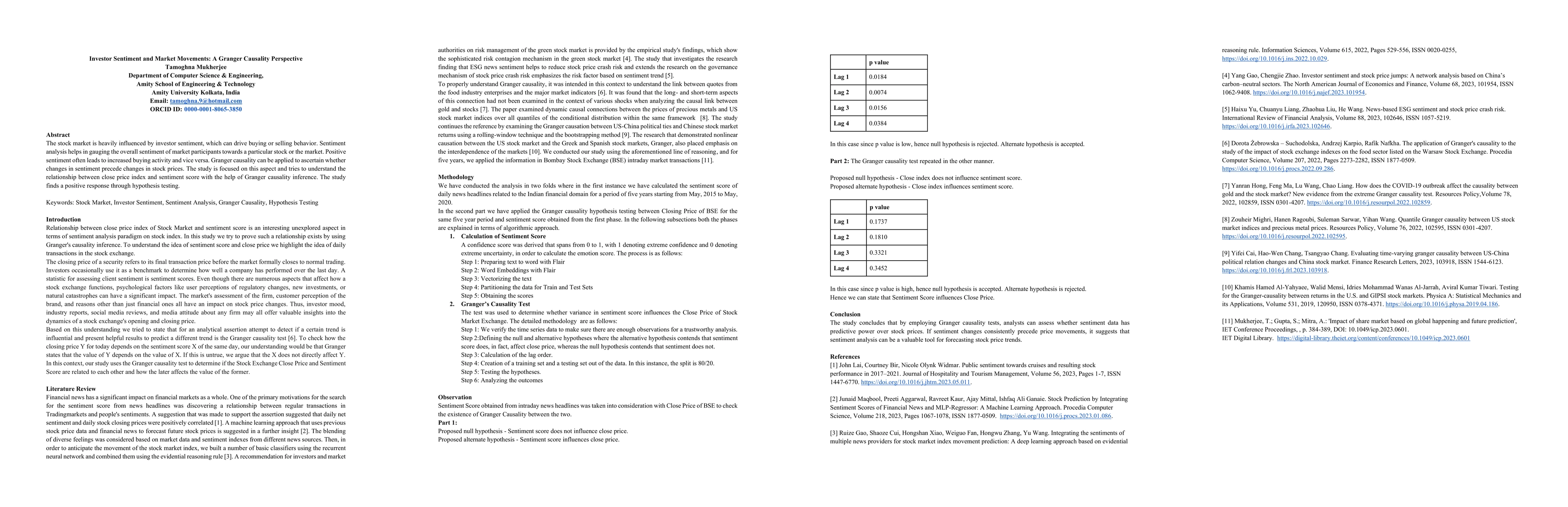

The study employed Granger causality tests to analyze the relationship between sentiment scores derived from financial news headlines and stock market close prices. Sentiment scores were calculated using text processing techniques, and hypothesis testing was conducted to determine causality.

Discussion 0