Publication

Metrics

AI Quick Summary

A new statistical model, k-Generalized Statistics, is proposed to analyze personal income distribution in Germany, Italy, and the UK, showing excellent agreement with observational data.

Paper Preview

Abstract

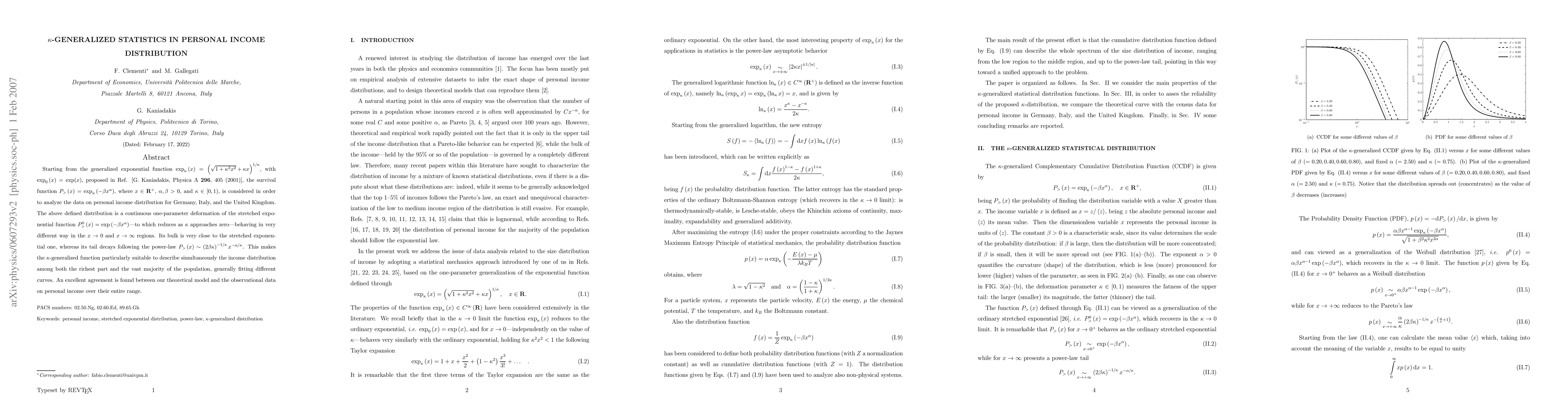

Starting from the generalized exponential function $\exp_{\kappa}(x)=(\sqrt{1+\kappa^{2}x^{2}}+\kappa x)^{1/\kappa}$, with $\exp_{0}(x)=\exp(x)$, proposed in Ref. [G. Kaniadakis, Physica A \textbf{296}, 405 (2001)], the survival function $P_{>}(x)=\exp_{\kappa}(-\beta x^{\alpha})$, where $x\in\mathbf{R}^{+}$, $\alpha,\beta>0$, and $\kappa\in[0,1)$, is considered in order to analyze the data on personal income distribution for Germany, Italy, and the United Kingdom. The above defined distribution is a continuous one-parameter deformation of the stretched exponential function $P_{>}^{0}(x)=\exp(-\beta x^{\alpha})$\textemdash to which reduces as $\kappa$ approaches zero\textemdash behaving in very different way in the $x\to0$ and $x\to\infty$ regions. Its bulk is very close to the stretched exponential one, whereas its tail decays following the power-law $P_{>}(x)\sim(2\beta\kappa)^{-1/\kappa}x^{-\alpha/\kappa}$. This makes the $\kappa$-generalized function particularly suitable to describe simultaneously the income distribution among both the richest part and the vast majority of the population, generally fitting different curves. An excellent agreement is found between our theoretical model and the observational data on personal income over their entire range.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0