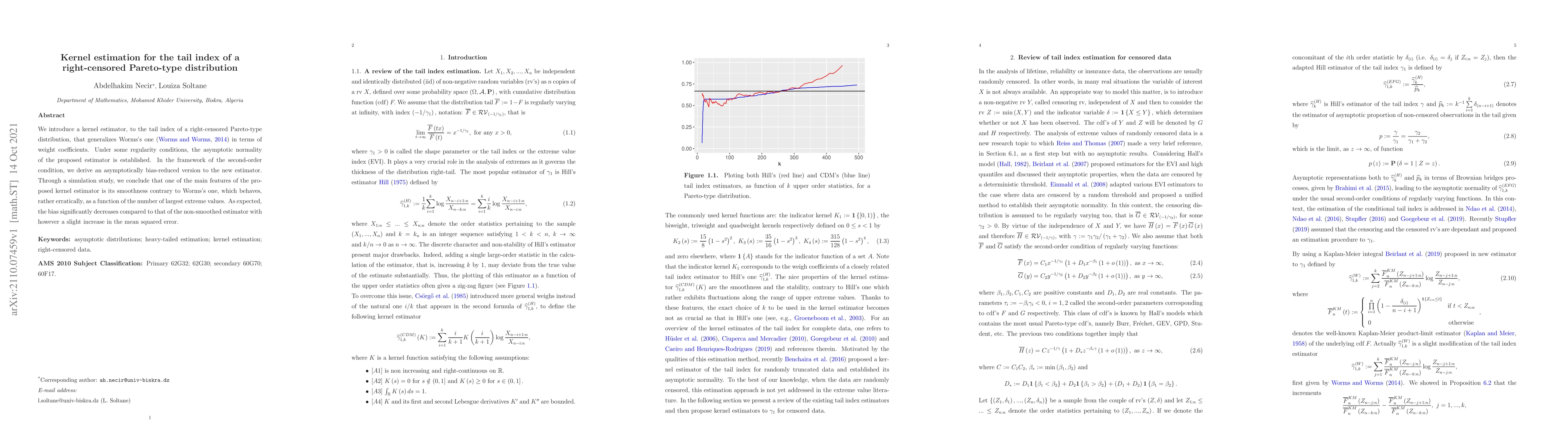

Kernel estimation for the tail index of a right-censored Pareto-type distribution

Publication

Metrics

AI Quick Summary

This paper proposes a kernel estimator for the tail index of right-censored Pareto-type distributions, improving upon Worms's estimator by incorporating weight coefficients. The new estimator demonstrates asymptotic normality and reduced bias under second-order conditions, though it slightly increases mean squared error, while maintaining smoother performance compared to the original estimator.

Paper Preview

Abstract

We introduce a kernel estimator, to the tail index of a right-censored Pareto-type distribution, that generalizes Worms's one (Worms and Worms, 2014)in terms of weight coefficients. Under some regularity conditions, the asymptotic normality of the proposed estimator is established. In the framework of the second-order condition, we derive an asymptotically bias-reduced version to the new estimator. Through a simulation study, we conclude that one of the main features of the proposed kernel estimator is its smoothness contrary to Worms's one, which behaves, rather erratically, as a function of the number of largest extreme values. As expected, the bias significantly decreases compared to that of the non-smoothed estimator with however a slight increase in the mean squared error.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0