Large-dimensional Factor Analysis without Moment Constraints

Publication

Metrics

AI Quick Summary

This paper introduces a novel method for estimating large-dimensional factor models without relying on moment constraints. It proposes using principal component analysis on the spatial Kendall's tau matrix, followed by ordinary least squares regression for factor scores. The method is shown to consistently estimate factor loadings, scores, and common components under elliptical distribution, with convergence rates provided. Simulations and a financial data analysis demonstrate its superior performance over classical PCA.

Paper Preview

Abstract

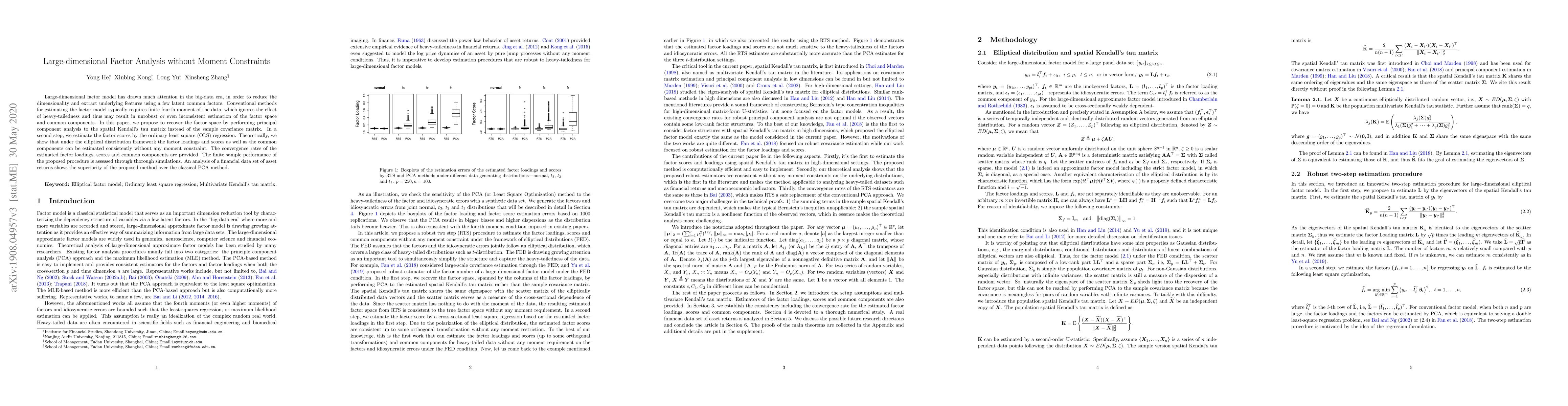

Large-dimensional factor model has drawn much attention in the big-data era, in order to reduce the dimensionality and extract underlying features using a few latent common factors. Conventional methods for estimating the factor model typically requires finite fourth moment of the data, which ignores the effect of heavy-tailedness and thus may result in unrobust or even inconsistent estimation of the factor space and common components. In this paper, we propose to recover the factor space by performing principal component analysis to the spatial Kendall's tau matrix instead of the sample covariance matrix. In a second step, we estimate the factor scores by the ordinary least square (OLS) regression. Theoretically, we show that under the elliptical distribution framework the factor loadings and scores as well as the common components can be estimated consistently without any moment constraint. The convergence rates of the estimated factor loadings, scores and common components are provided. The finite sample performance of the proposed procedure is assessed through thorough simulations. An analysis of a financial data set of asset returns shows the superiority of the proposed method over the classical PCA method.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0