Latent Structural Similarity Networks for Unsupervised Discovery in Multivariate Time Series

Publication

Metrics

Paper Preview

Abstract

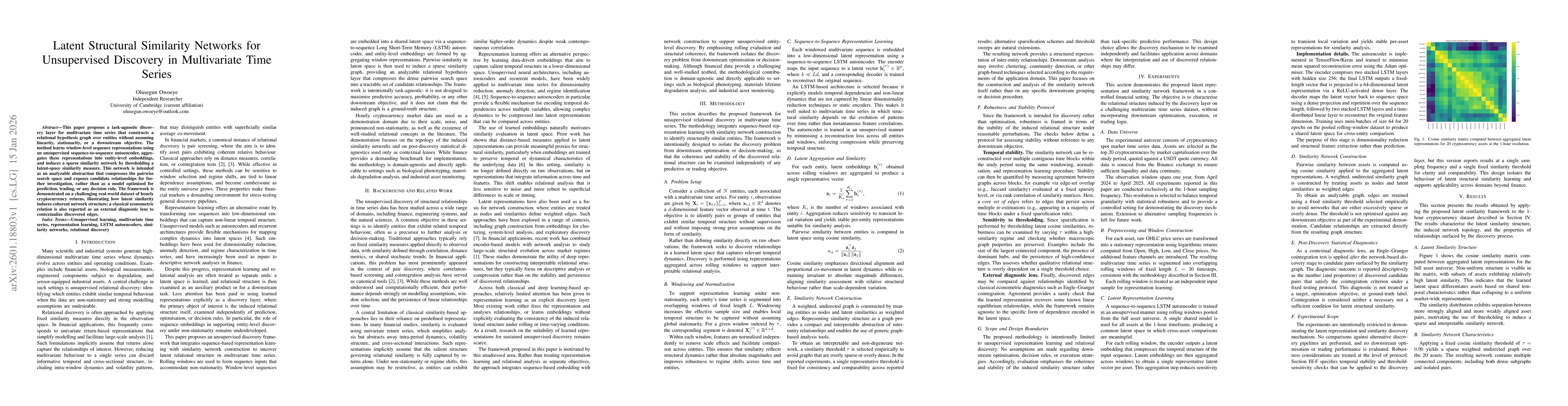

This paper proposes a task-agnostic discovery layer for multivariate time series that constructs a relational hypothesis graph over entities without assuming linearity, stationarity, or a downstream objective. The method learns window-level sequence representations using an unsupervised sequence-to-sequence autoencoder, aggregates these representations into entity-level embeddings, and induces a sparse similarity network by thresholding a latent-space similarity measure. This network is intended as an analyzable abstraction that compresses the pairwise search space and exposes candidate relationships for further investigation, rather than as a model optimized for prediction, trading, or any decision rule. The framework is demonstrated on a challenging real-world dataset of hourly cryptocurrency returns, illustrating how latent similarity induces coherent network structure; a classical econometric relation is also reported as an external diagnostic lens to contextualize discovered edges.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0