Learning and Decision-Making with Data: Optimal Formulations and Phase Transitions

Publication

Metrics

AI Quick Summary

This paper proposes a novel approach to designing optimal data-driven formulations for learning and decision-making, balancing estimated cost proximity and out-of-sample performance. It identifies three distinct performance regimes where optimal formulations transition from robust to entropic to variance-penalized, revealing hidden connections between seemingly different formulations.

Paper Preview

Abstract

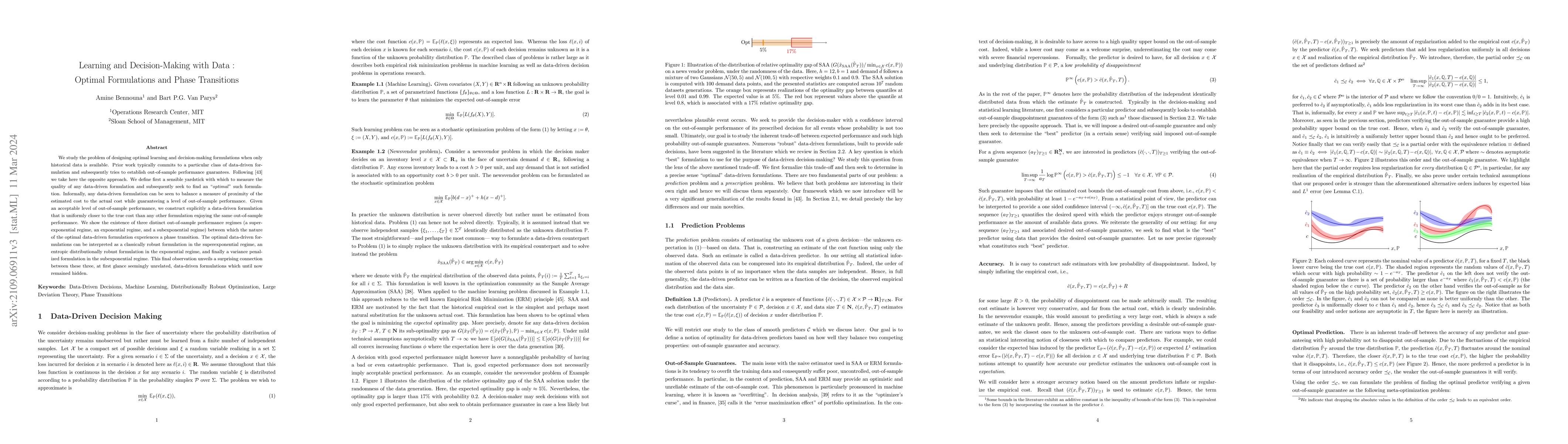

We study the problem of designing optimal learning and decision-making formulations when only historical data is available. Prior work typically commits to a particular class of data-driven formulation and subsequently tries to establish out-of-sample performance guarantees. We take here the opposite approach. We define first a sensible yard stick with which to measure the quality of any data-driven formulation and subsequently seek to find an optimal such formulation. Informally, any data-driven formulation can be seen to balance a measure of proximity of the estimated cost to the actual cost while guaranteeing a level of out-of-sample performance. Given an acceptable level of out-of-sample performance, we construct explicitly a data-driven formulation that is uniformly closer to the true cost than any other formulation enjoying the same out-of-sample performance. We show the existence of three distinct out-of-sample performance regimes (a superexponential regime, an exponential regime and a subexponential regime) between which the nature of the optimal data-driven formulation experiences a phase transition. The optimal data-driven formulations can be interpreted as a classically robust formulation in the superexponential regime, an entropic distributionally robust formulation in the exponential regime and finally a variance penalized formulation in the subexponential regime. This final observation unveils a surprising connection between these three, at first glance seemingly unrelated, data-driven formulations which until now remained hidden.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0