Learning Latent Representations of Bank Customers With The Variational Autoencoder

Publication

Metrics

AI Quick Summary

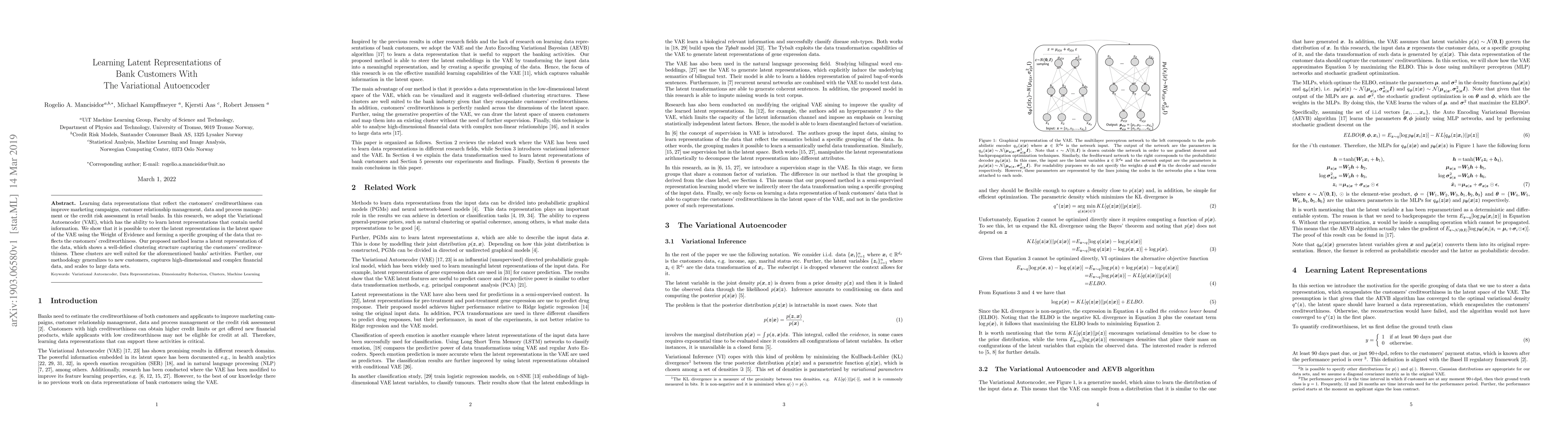

This research employs a Variational Autoencoder (VAE) to learn latent representations of bank customers that reflect their creditworthiness, enhancing marketing and risk assessment. The method successfully clusters customers based on creditworthiness and generalizes to new data, scaling effectively for large datasets.

Paper Preview

Abstract

Learning data representations that reflect the customers' creditworthiness can improve marketing campaigns, customer relationship management, data and process management or the credit risk assessment in retail banks. In this research, we adopt the Variational Autoencoder (VAE), which has the ability to learn latent representations that contain useful information. We show that it is possible to steer the latent representations in the latent space of the VAE using the Weight of Evidence and forming a specific grouping of the data that reflects the customers' creditworthiness. Our proposed method learns a latent representation of the data, which shows a well-defied clustering structure capturing the customers' creditworthiness. These clusters are well suited for the aforementioned banks' activities. Further, our methodology generalizes to new customers, captures high-dimensional and complex financial data, and scales to large data sets.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0