Publication

Metrics

Paper Preview

Abstract

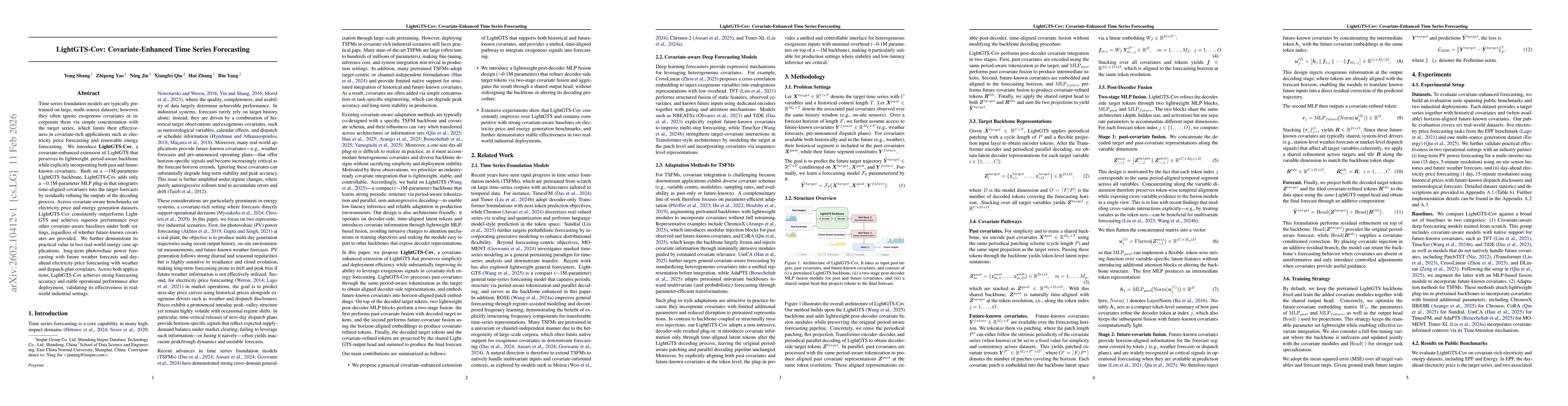

Time series foundation models are typically pre-trained on large, multi-source datasets; however, they often ignore exogenous covariates or incorporate them via simple concatenation with the target series, which limits their effectiveness in covariate-rich applications such as electricity price forecasting and renewable energy forecasting. We introduce LightGTS-Cov, a covariate-enhanced extension of LightGTS that preserves its lightweight, period-aware backbone while explicitly incorporating both past and future-known covariates. Built on a $\sim$1M-parameter LightGTS backbone, LightGTS-Cov adds only a $\sim$0.1M-parameter MLP plug-in that integrates time-aligned covariates into the target forecasts by residually refining the outputs of the decoding process. Across covariate-aware benchmarks on electricity price and energy generation datasets, LightGTS-Cov consistently outperforms LightGTS and achieves superior performance over other covariate-aware baselines under both settings, regardless of whether future-known covariates are provided. We further demonstrate its practical value in two real-world energy case applications: long-term photovoltaic power forecasting with future weather forecasts and day-ahead electricity price forecasting with weather and dispatch-plan covariates. Across both applications, LightGTS-Cov achieves strong forecasting accuracy and stable operational performance after deployment, validating its effectiveness in real-world industrial settings.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0