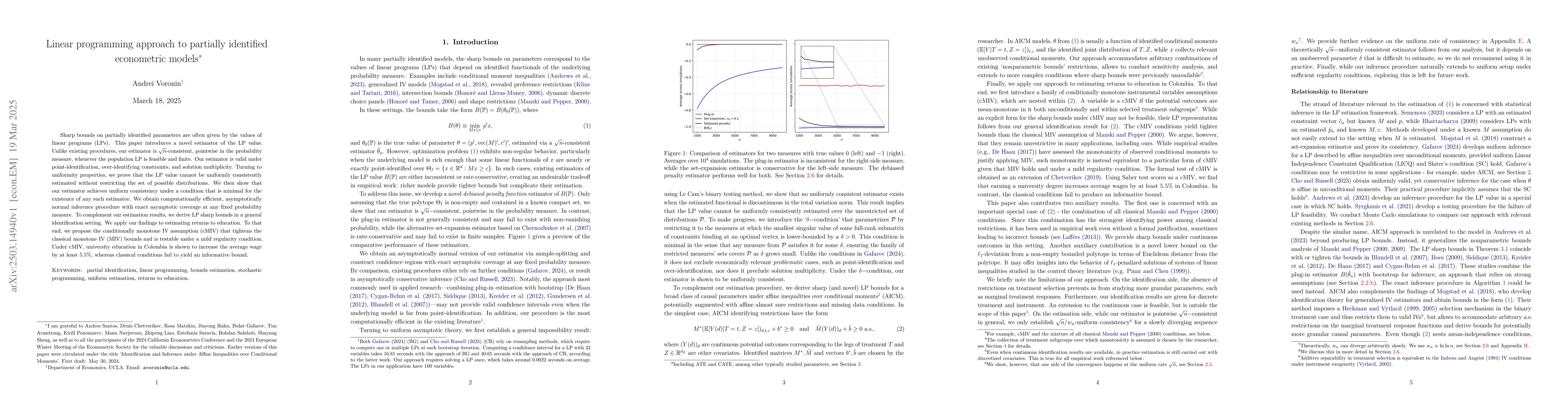

Sharp bounds on partially identified parameters are often given by the values

of linear programs (LPs). This paper introduces a novel estimator of the LP

value. Unlike existing procedures, our estimator is root-n-consistent,

pointwise in the probability measure, whenever the population LP is feasible

and finite. Our estimator is valid under point-identification, over-identifying

constraints, and solution multiplicity. Turning to uniformity properties, we

prove that the LP value cannot be uniformly consistently estimated without

restricting the set of possible distributions. We then show that our estimator

achieves uniform consistency under a condition that is minimal for the

existence of any such estimator. We obtain computationally efficient,

asymptotically normal inference procedure with exact asymptotic coverage at any

fixed probability measure. To complement our estimation results, we derive LP

sharp bounds in a general identification setting. We apply our findings to

estimating returns to education. To that end, we propose the conditionally

monotone IV assumption (cMIV) that tightens the classical monotone IV (MIV)

bounds and is testable under a mild regularity condition. Under cMIV,

university education in Colombia is shown to increase the average wage by at

least $5.5\%$, whereas classical conditions fail to yield an informative bound.

Discussion 0