Liquidation, Leverage and Optimal Margin in Bitcoin Futures Markets

Publication

Metrics

AI Quick Summary

This paper uses extreme value theory to analyze liquidation, leverage, and optimal margins in Bitcoin futures markets. Findings indicate significant daily forced liquidations and high leverage among traders, suggesting that current 1% margin requirements are insufficient and should be increased to 33% for long and 20% for short positions to reduce margin call risks.

Paper Preview

Abstract

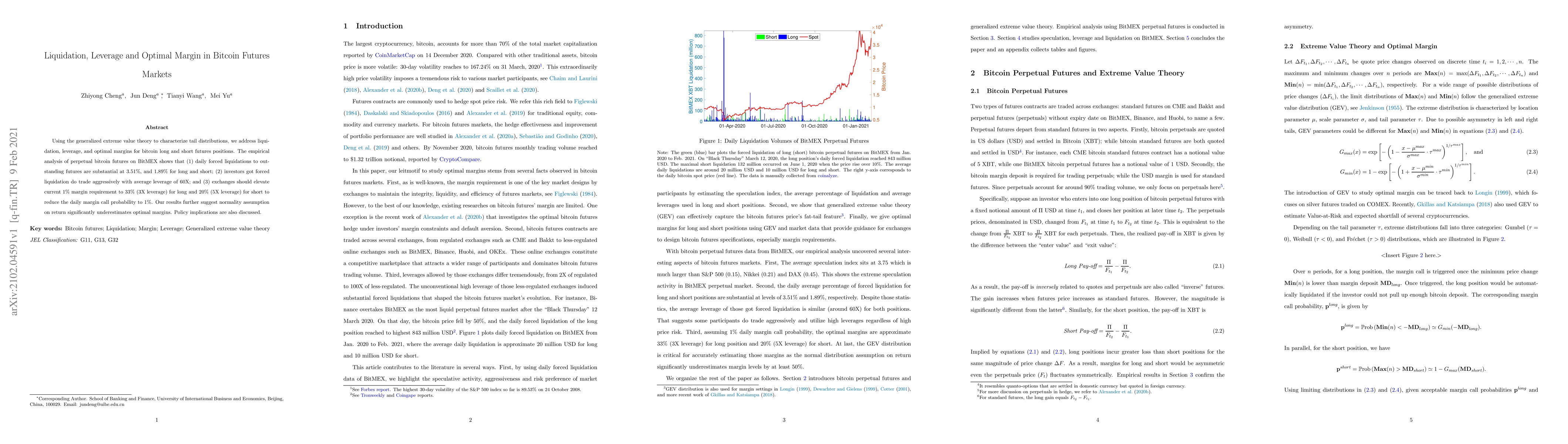

Using the generalized extreme value theory to characterize tail distributions, we address liquidation, leverage, and optimal margins for bitcoin long and short futures positions. The empirical analysis of perpetual bitcoin futures on BitMEX shows that (1) daily forced liquidations to out- standing futures are substantial at 3.51%, and 1.89% for long and short; (2) investors got forced liquidation do trade aggressively with average leverage of 60X; and (3) exchanges should elevate current 1% margin requirement to 33% (3X leverage) for long and 20% (5X leverage) for short to reduce the daily margin call probability to 1%. Our results further suggest normality assumption on return significantly underestimates optimal margins. Policy implications are also discussed.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0