Local Control Regression: Improving the Least Squares Monte Carlo Method for Portfolio Optimization

Publication

Metrics

AI Quick Summary

This paper proposes a local control regression method to improve the least squares Monte Carlo algorithm for portfolio optimization, demonstrating that using adaptive, coarse grids for local regression can yield accurate results with reduced computational cost compared to global control regression.

Paper Preview

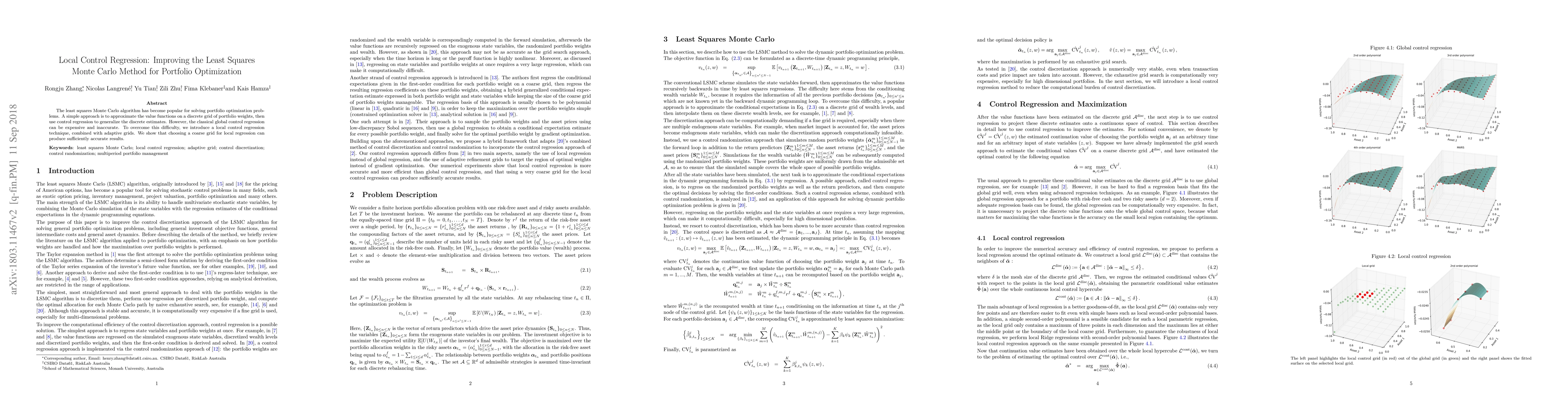

Abstract

The least squares Monte Carlo algorithm has become popular for solving portfolio optimization problems. A simple approach is to approximate the value functions on a discrete grid of portfolio weights, then use control regression to generalize the discrete estimates. However, the classical global control regression can be expensive and inaccurate. To overcome this difficulty, we introduce a local control regression technique, combined with adaptive grids. We show that choosing a coarse grid for local regression can produce sufficiently accurate results.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0