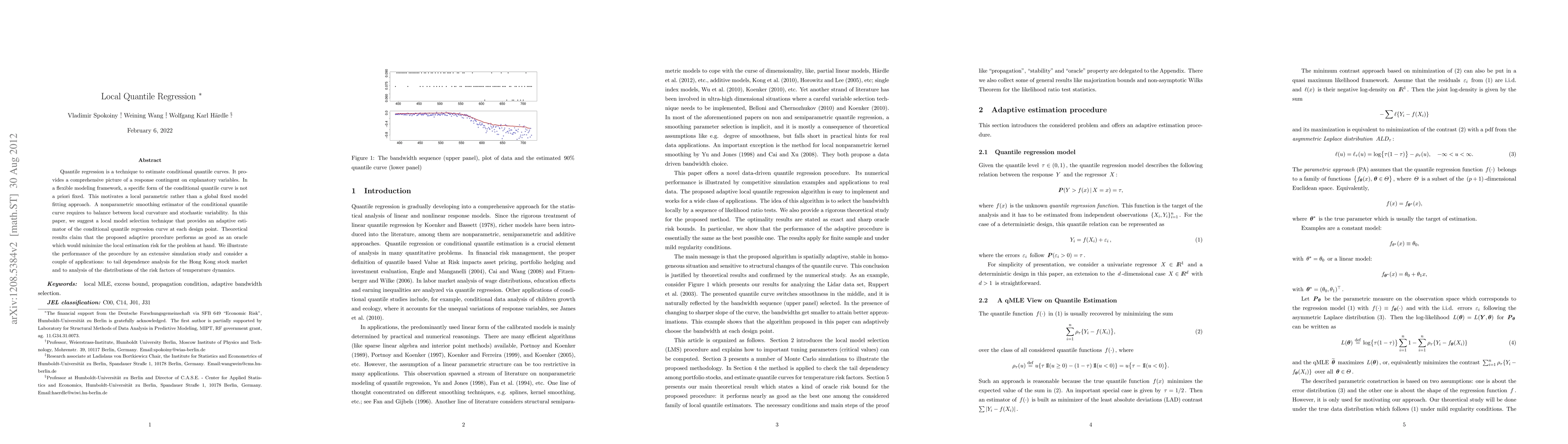

Quantile regression is a technique to estimate conditional quantile curves.

It provides a comprehensive picture of a response contingent on explanatory

variables. In a flexible modeling framework, a specific form of the conditional

quantile curve is not a priori fixed. % Indeed, the majority of applications do

not per se require specific functional forms. This motivates a local parametric

rather than a global fixed model fitting approach. A nonparametric smoothing

estimator of the conditional quantile curve requires to balance between local

curvature and stochastic variability. In this paper, we suggest a local model

selection technique that provides an adaptive estimator of the conditional

quantile regression curve at each design point. Theoretical results claim that

the proposed adaptive procedure performs as good as an oracle which would

minimize the local estimation risk for the problem at hand. We illustrate the

performance of the procedure by an extensive simulation study and consider a

couple of applications: to tail dependence analysis for the Hong Kong stock

market and to analysis of the distributions of the risk factors of temperature

dynamics.

Discussion 0