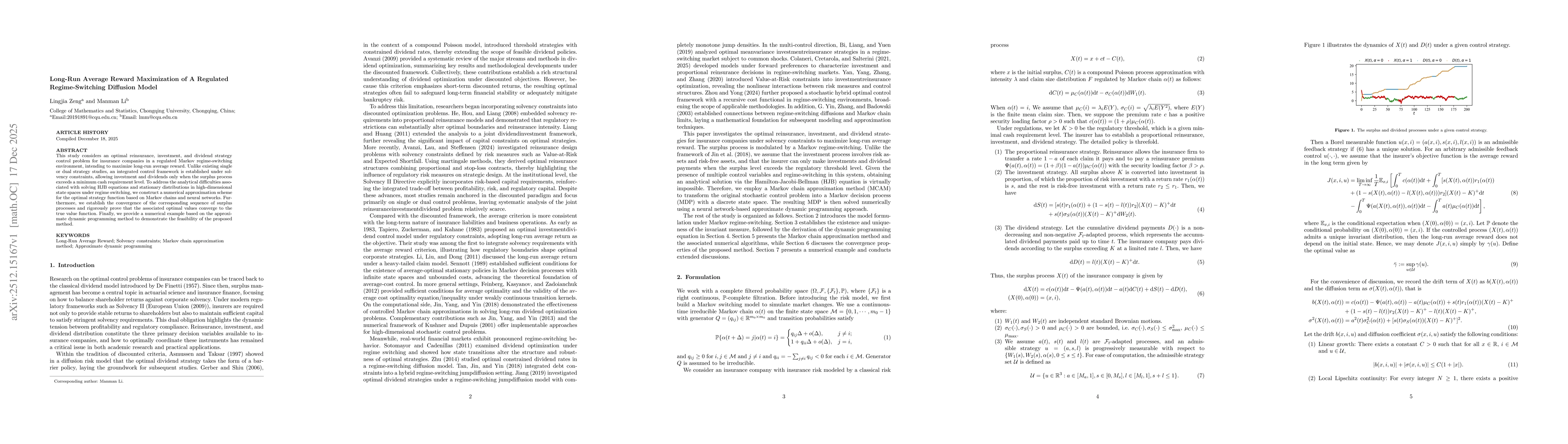

This study considers an optimal reinsurance, investment, and dividend strategy control problem for insurance companies in a regulated Markov regime-switching environment, intending to maximize long-run average reward. Unlike existing single or dual strategy studies, an integrated control framework is established under solvency constraints, allowing investment and dividends only when the surplus process exceeds a minimum cash requirement level. To address the analytical difficulties associated with solving HJB equations and stationary distributions in high-dimensional state spaces under regime switching, we construct a numerical approximation scheme for the optimal strategy function based on Markov chains and neural networks. Furthermore, we establish the convergence of the corresponding sequence of surplus processes and rigorously prove that the associated optimal values converge to the true value function. Finally, we provide a numerical example based on the approximate dynamic programming method to demonstrate the feasibility of the proposed method.

Discussion 0