Long-term Memory and Volatility Clustering in Daily and High-frequency Price Changes

Publication

Metrics

AI Quick Summary

The research examines long-term memory in stock market indices and FX rates, finding no such memory in return series but a strong property in volatility time series. Using DFA, AR(1) and GARCH(1,1) models, the study concludes that volatility clustering causes the long-term memory in financial time series, with findings consistent across daily and high-frequency data.

Paper Preview

Abstract

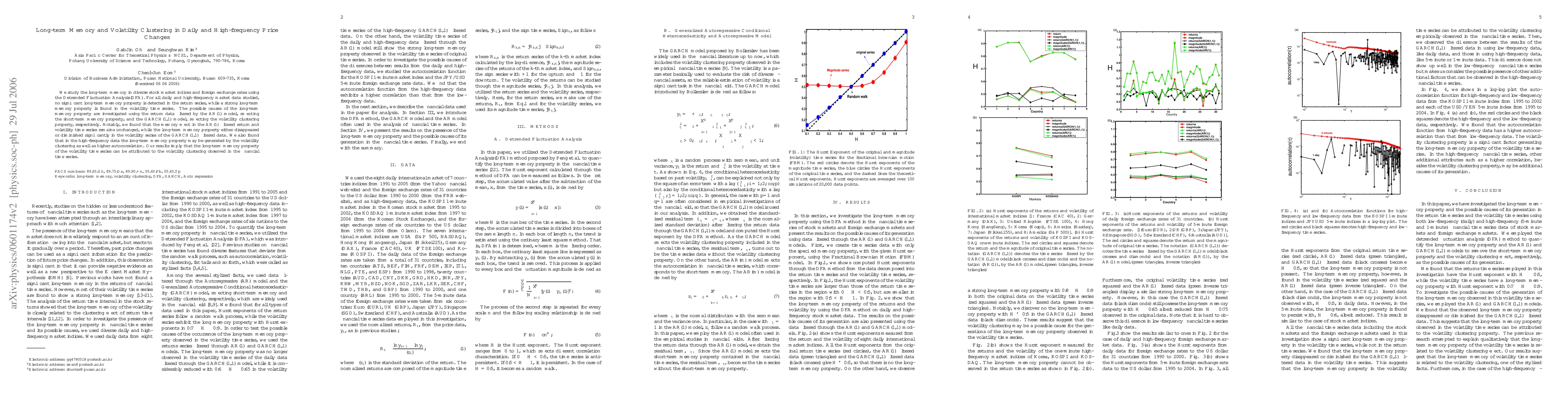

We study the long-term memory in diverse stock market indices and foreign exchange rates using the Detrended Fluctuation Analysis(DFA). For all daily and high-frequency market data studied, no significant long-term memory property is detected in the return series, while a strong long-term memory property is found in the volatility time series. The possible causes of the long-term memory property are investigated using the return data filtered by the AR(1) model, reflecting the short-term memory property, and the GARCH(1,1) model, reflecting the volatility clustering property, respectively. Notably, we found that the memory effect in the AR(1) filtered return and volatility time series remains unchanged, while the long-term memory property either disappeared or diminished significantly in the volatility series of the GARCH(1,1) filtered data. We also found that in the high-frequency data the long-term memory property may be generated by the volatility clustering as well as higher autocorrelation. Our results imply that the long-term memory property of the volatility time series can be attributed to the volatility clustering observed in the financial time series.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Discussion 0