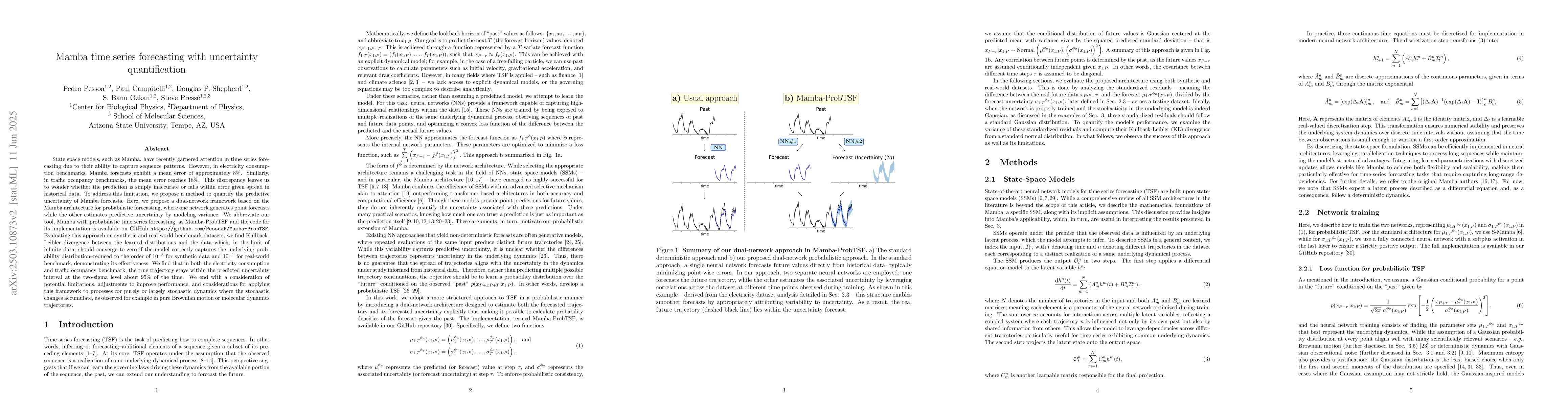

State space models, such as Mamba, have recently garnered attention in time

series forecasting due to their ability to capture sequence patterns. However,

in electricity consumption benchmarks, Mamba forecasts exhibit a mean error of

approximately 8\%. Similarly, in traffic occupancy benchmarks, the mean error

reaches 18\%. This discrepancy leaves us to wonder whether the prediction is

simply inaccurate or falls within error given spread in historical data. To

address this limitation, we propose a method to quantify the predictive

uncertainty of Mamba forecasts. Here, we propose a dual-network framework based

on the Mamba architecture for probabilistic forecasting, where one network

generates point forecasts while the other estimates predictive uncertainty by

modeling variance. We abbreviate our tool, Mamba with probabilistic time series

forecasting, as Mamba-ProbTSF and the code for its implementation is available

on GitHub (https://github.com/PessoaP/Mamba-ProbTSF). Evaluating this approach

on synthetic and real-world benchmark datasets, we find Kullback-Leibler

divergence between the learned distributions and the data--which, in the limit

of infinite data, should converge to zero if the model correctly captures the

underlying probability distribution--reduced to the order of $10^{-3}$ for

synthetic data and $10^{-1}$ for real-world benchmark, demonstrating its

effectiveness. We find that in both the electricity consumption and traffic

occupancy benchmark, the true trajectory stays within the predicted uncertainty

interval at the two-sigma level about 95\% of the time. We end with a

consideration of potential limitations, adjustments to improve performance, and

considerations for applying this framework to processes for purely or largely

stochastic dynamics where the stochastic changes accumulate, as observed for

example in pure Brownian motion or molecular dynamics trajectories.

Discussion 0