Manifold Feature Index: A novel index based on high-dimensional data simplification

Publication

Metrics

AI Quick Summary

A new stock index model called the Manifold Feature (MF) index is proposed to reflect market activity, offering closer data approximation and higher stability than traditional indices.

Paper Preview

Abstract

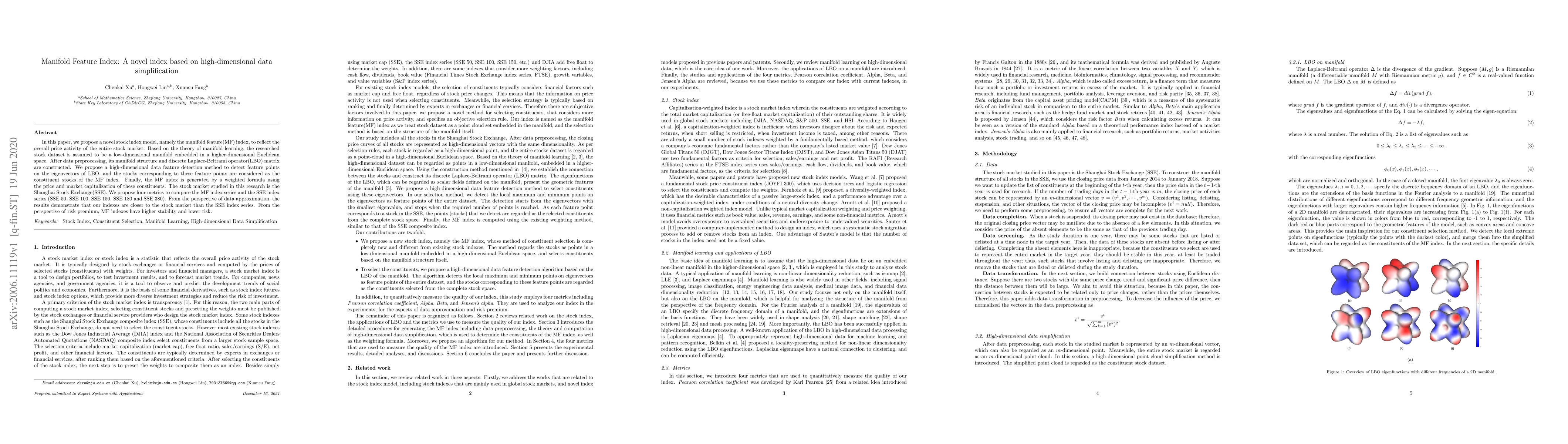

In this paper, we propose a novel stock index model, namely the manifold feature(MF) index, to reflect the overall price activity of the entire stock market. Based on the theory of manifold learning, the researched stock dataset is assumed to be a low-dimensional manifold embedded in a higher-dimensional Euclidean space. After data preprocessing, its manifold structure and discrete Laplace-Beltrami operator(LBO) matrix are constructed. We propose a high-dimensional data feature detection method to detect feature points on the eigenvectors of LBO, and the stocks corresponding to these feature points are considered as the constituent stocks of the MF index. Finally, the MF index is generated by a weighted formula using the price and market capitalization of these constituents. The stock market studied in this research is the Shanghai Stock Exchange(SSE). We propose four metrics to compare the MF index series and the SSE index series (SSE 50, SSE 100, SSE 150, SSE 180 and SSE 380). From the perspective of data approximation, the results demonstrate that our indexes are closer to the stock market than the SSE index series. From the perspective of risk premium, MF indexes have higher stability and lower risk.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0