01

MethodologyHow they did it

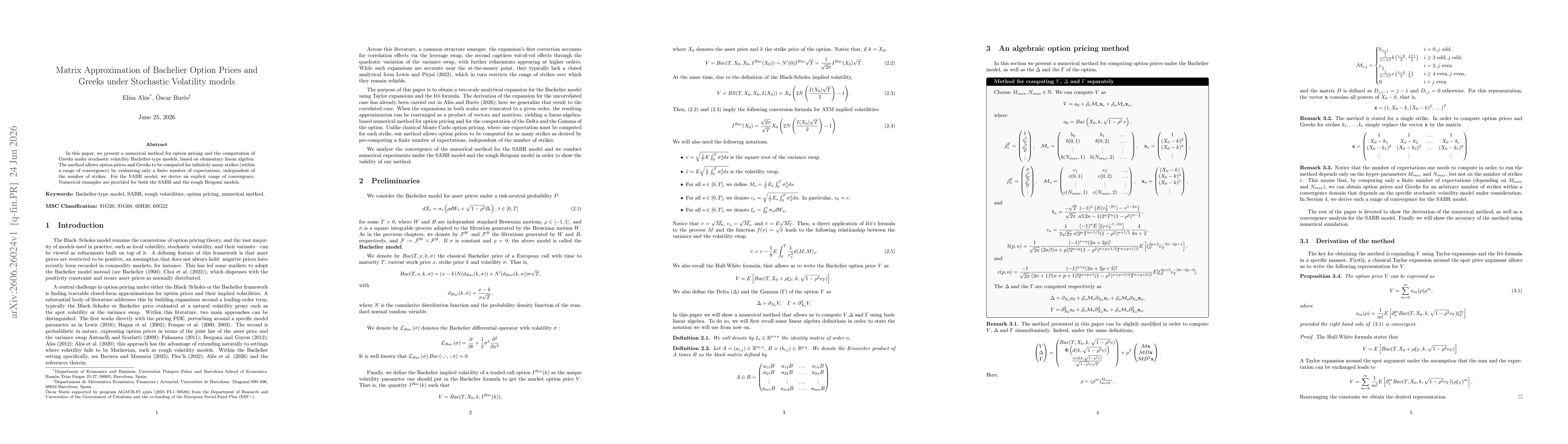

The paper develops a linear-algebra-based numerical method that expresses two-scale Taylor expansions and Itô calculus for the Bachelier model under stochastic volatility, enabling pricing and Greeks computation for infinitely many strikes within a convergence range by precomputing a finite set of expectations. It extends the approach to correlated cases and demonstrates convergence analysis specifically for the SABR model, supported by numerical experiments on SABR and rough Bergomi models.

Discussion 0