Publication

Metrics

Paper Preview

Abstract

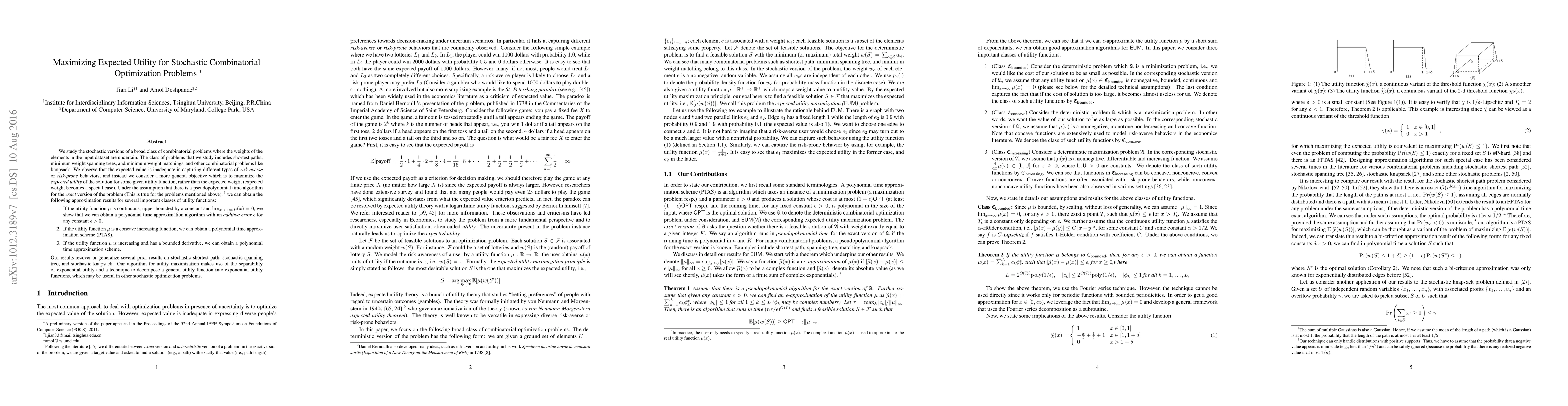

We study the stochastic versions of a broad class of combinatorial problems where the weights of the elements in the input dataset are uncertain. The class of problems that we study includes shortest paths, minimum weight spanning trees, and minimum weight matchings, and other combinatorial problems like knapsack. We observe that the expected value is inadequate in capturing different types of {\em risk-averse} or {\em risk-prone} behaviors, and instead we consider a more general objective which is to maximize the {\em expected utility} of the solution for some given utility function, rather than the expected weight (expected weight becomes a special case). Under the assumption that there is a pseudopolynomial time algorithm for the {\em exact} version of the problem (This is true for the problems mentioned above), we can obtain the following approximation results for several important classes of utility functions: (1) If the utility function $\uti$ is continuous, upper-bounded by a constant and $\lim_{x\rightarrow+\infty}\uti(x)=0$, we show that we can obtain a polynomial time approximation algorithm with an {\em additive error} $\epsilon$ for any constant $\epsilon>0$. (2) If the utility function $\uti$ is a concave increasing function, we can obtain a polynomial time approximation scheme (PTAS). (3) If the utility function $\uti$ is increasing and has a bounded derivative, we can obtain a polynomial time approximation scheme. Our results recover or generalize several prior results on stochastic shortest path, stochastic spanning tree, and stochastic knapsack. Our algorithm for utility maximization makes use of the separability of exponential utility and a technique to decompose a general utility function into exponential utility functions, which may be useful in other stochastic optimization problems.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0