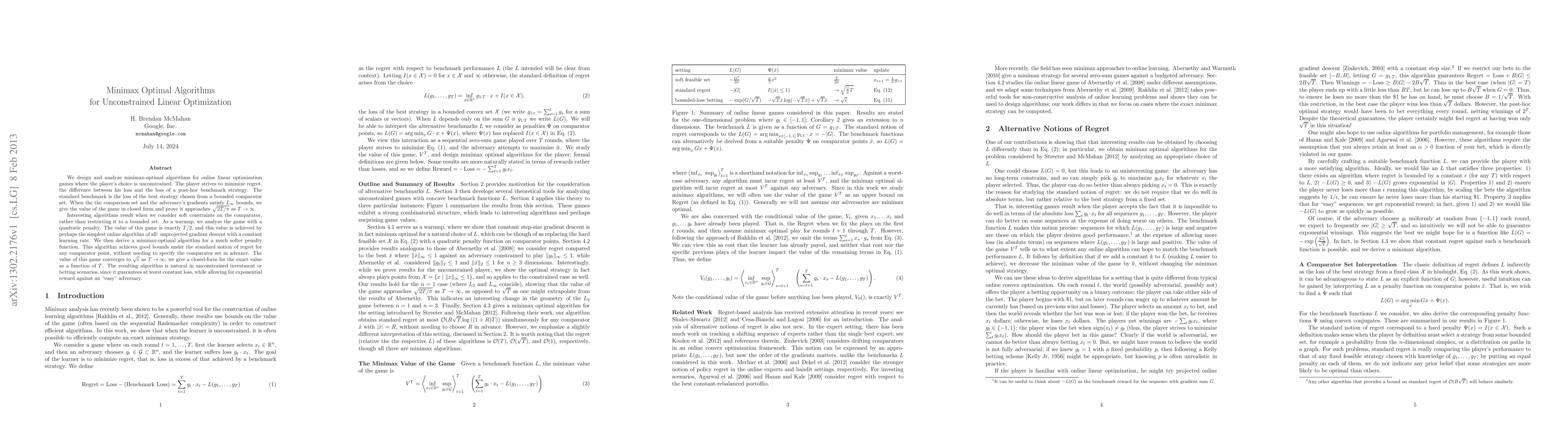

Minimax Optimal Algorithms for Unconstrained Linear Optimization

Publication

Metrics

AI Quick Summary

This paper develops minimax-optimal algorithms for online linear optimization, focusing on minimizing regret against a post-hoc benchmark. It finds that under L_infinity bounds, the game's value approaches sqrt(2T/pi) as the number of rounds T increases. The study also introduces an algorithm achieving a value of T/2 under a quadratic penalty, and a softer penalty algorithm converging to sqrt{e} with a closed-form exact value.

Paper Preview

Abstract

We design and analyze minimax-optimal algorithms for online linear optimization games where the player's choice is unconstrained. The player strives to minimize regret, the difference between his loss and the loss of a post-hoc benchmark strategy. The standard benchmark is the loss of the best strategy chosen from a bounded comparator set. When the the comparison set and the adversary's gradients satisfy L_infinity bounds, we give the value of the game in closed form and prove it approaches sqrt(2T/pi) as T -> infinity. Interesting algorithms result when we consider soft constraints on the comparator, rather than restricting it to a bounded set. As a warmup, we analyze the game with a quadratic penalty. The value of this game is exactly T/2, and this value is achieved by perhaps the simplest online algorithm of all: unprojected gradient descent with a constant learning rate. We then derive a minimax-optimal algorithm for a much softer penalty function. This algorithm achieves good bounds under the standard notion of regret for any comparator point, without needing to specify the comparator set in advance. The value of this game converges to sqrt{e} as T ->infinity; we give a closed-form for the exact value as a function of T. The resulting algorithm is natural in unconstrained investment or betting scenarios, since it guarantees at worst constant loss, while allowing for exponential reward against an "easy" adversary.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0