Model-Free Reinforcement Learning for Financial Portfolios: A Brief Survey

Publication

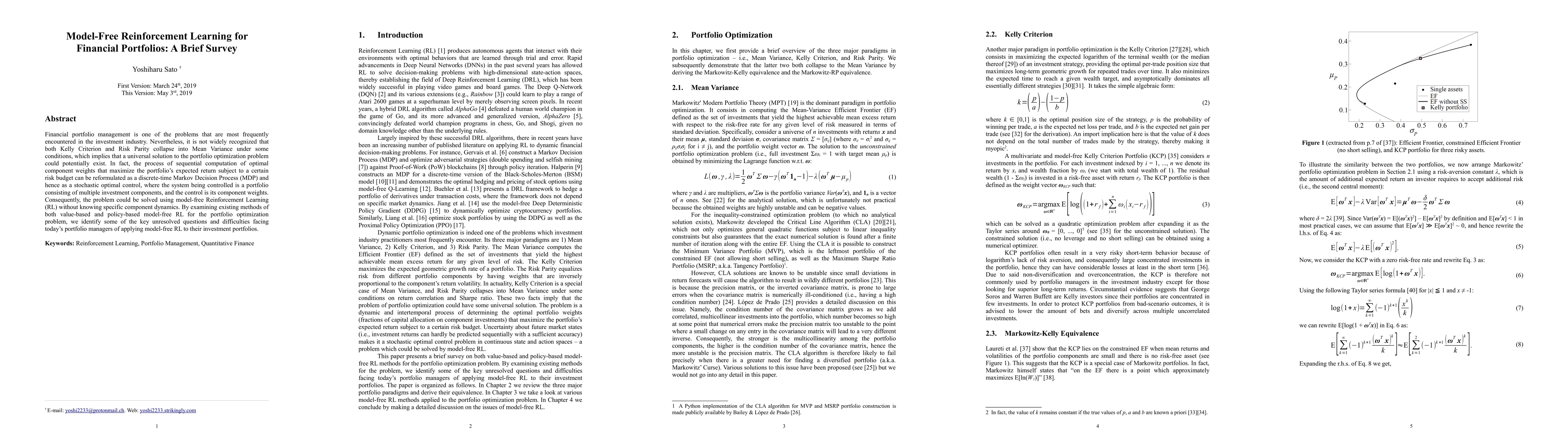

Metrics

Paper Preview

Abstract

Financial portfolio management is one of the problems that are most frequently encountered in the investment industry. Nevertheless, it is not widely recognized that both Kelly Criterion and Risk Parity collapse into Mean Variance under some conditions, which implies that a universal solution to the portfolio optimization problem could potentially exist. In fact, the process of sequential computation of optimal component weights that maximize the portfolio's expected return subject to a certain risk budget can be reformulated as a discrete-time Markov Decision Process (MDP) and hence as a stochastic optimal control, where the system being controlled is a portfolio consisting of multiple investment components, and the control is its component weights. Consequently, the problem could be solved using model-free Reinforcement Learning (RL) without knowing specific component dynamics. By examining existing methods of both value-based and policy-based model-free RL for the portfolio optimization problem, we identify some of the key unresolved questions and difficulties facing today's portfolio managers of applying model-free RL to their investment portfolios.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0