Publication

Metrics

AI Quick Summary

This paper introduces a new neural network architecture for modeling multivariate extreme value distributions, enabling non-parametric calibration and generation of these distributions while preserving essential shape constraints. The approach approximates the dependence structure encoded by these distributions at parametric rates and demonstrates its effectiveness in various experimental settings.

Paper Preview

Abstract

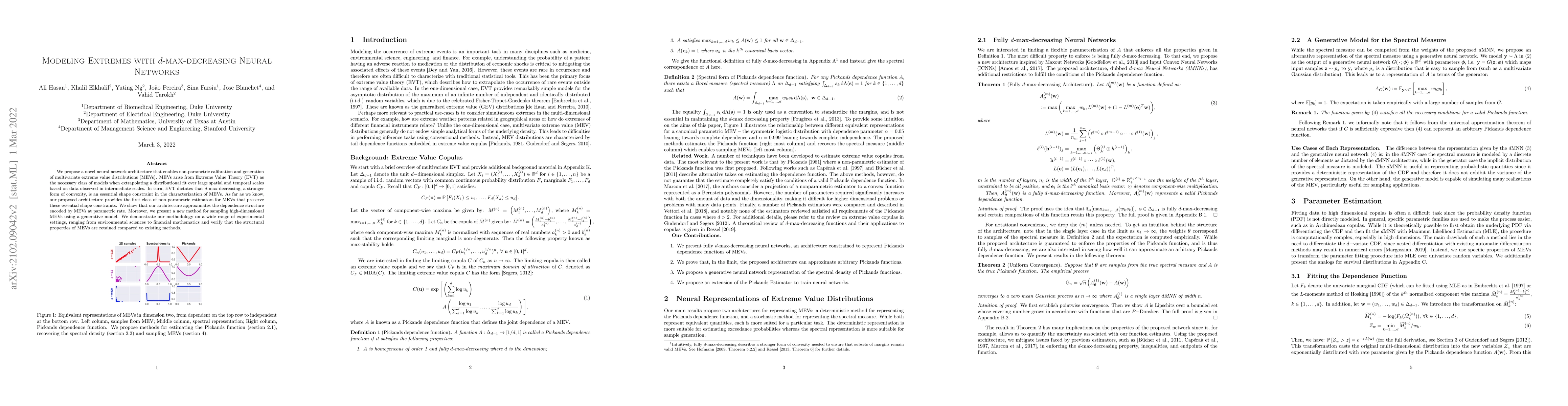

We propose a novel neural network architecture that enables non-parametric calibration and generation of multivariate extreme value distributions (MEVs). MEVs arise from Extreme Value Theory (EVT) as the necessary class of models when extrapolating a distributional fit over large spatial and temporal scales based on data observed in intermediate scales. In turn, EVT dictates that $d$-max-decreasing, a stronger form of convexity, is an essential shape constraint in the characterization of MEVs. As far as we know, our proposed architecture provides the first class of non-parametric estimators for MEVs that preserve these essential shape constraints. We show that our architecture approximates the dependence structure encoded by MEVs at parametric rate. Moreover, we present a new method for sampling high-dimensional MEVs using a generative model. We demonstrate our methodology on a wide range of experimental settings, ranging from environmental sciences to financial mathematics and verify that the structural properties of MEVs are retained compared to existing methods.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0