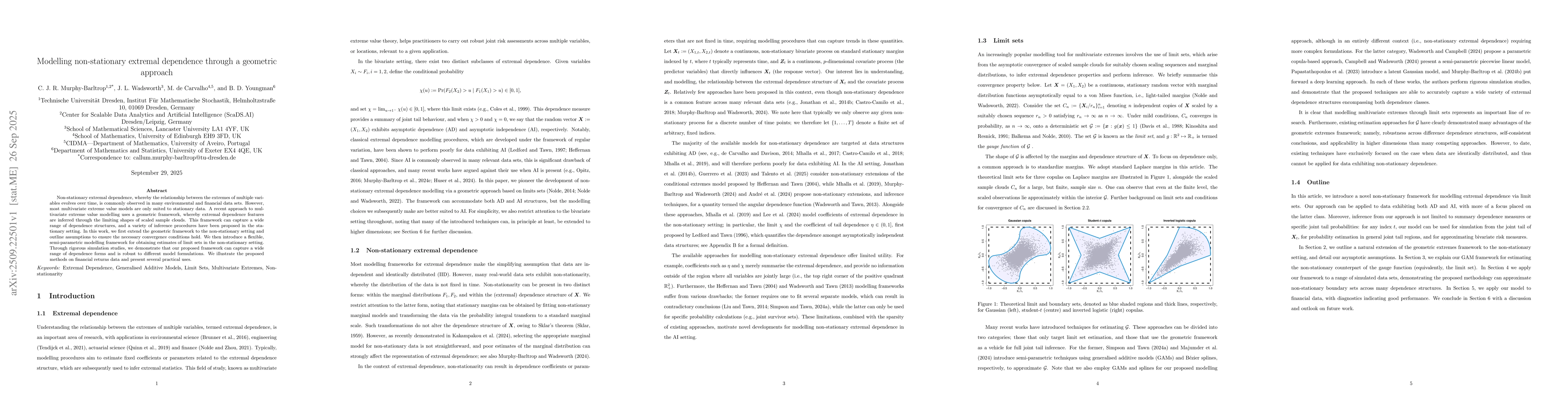

Non-stationary extremal dependence, whereby the relationship between the

extremes of multiple variables evolves over time, is commonly observed in many

environmental and financial data sets. However, most multivariate extreme value

models are only suited to stationary data. A recent approach to multivariate

extreme value modelling uses a geometric framework, whereby extremal dependence

features are inferred through the limiting shapes of scaled sample clouds. This

framework can capture a wide range of dependence structures, and a variety of

inference procedures have been proposed in the stationary setting. In this

work, we first extend the geometric framework to the non-stationary setting and

outline assumptions to ensure the necessary convergence conditions hold. We

then introduce a flexible, semi-parametric modelling framework for obtaining

estimates of limit sets in the non-stationary setting. Through rigorous

simulation studies, we demonstrate that our proposed framework can capture a

wide range of dependence forms and is robust to different model formulations.

We illustrate the proposed methods on financial returns data and present

several practical uses.

Discussion 0