Modelling volatile time series with v-transforms and copulas

Publication

Metrics

AI Quick Summary

This paper proposes a novel modelling approach for volatile time series using v-transforms and copulas, which link the quantiles of the time series to a volatility proxy. The model combines arbitrary marginal distributions with copula processes for volatility dynamics, illustrated with a Gaussian ARMA copula, and is shown to replicate financial return series characteristics and facilitate risk measures, outperforming standard GARCH in Bitcoin return data.

Paper Preview

Abstract

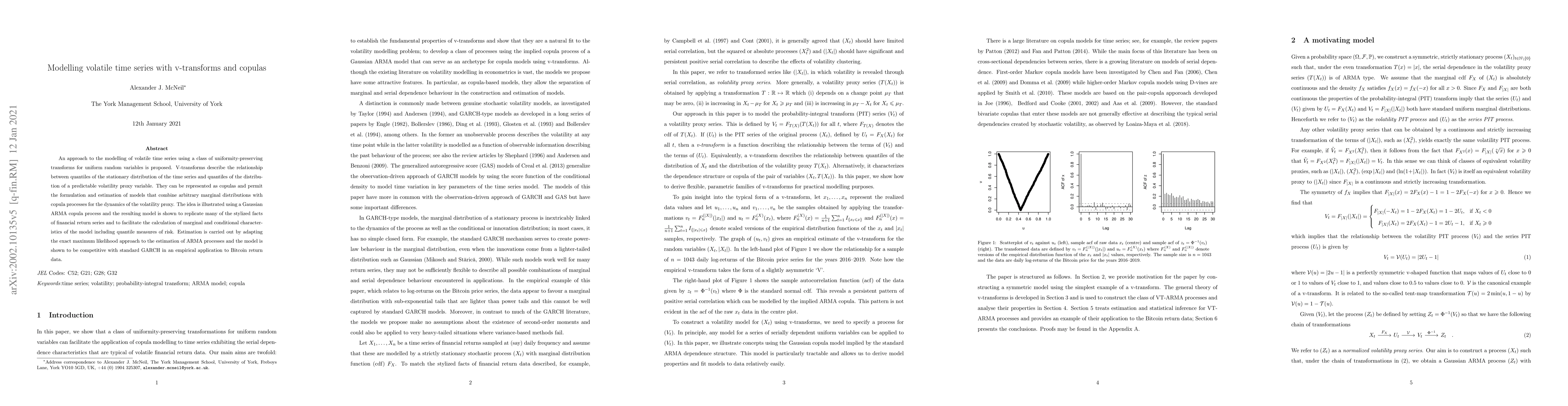

An approach to the modelling of volatile time series using a class of uniformity-preserving transforms for uniform random variables is proposed. V-transforms describe the relationship between quantiles of the stationary distribution of the time series and quantiles of the distribution of a predictable volatility proxy variable. They can be represented as copulas and permit the formulation and estimation of models that combine arbitrary marginal distributions with copula processes for the dynamics of the volatility proxy. The idea is illustrated using a Gaussian ARMA copula process and the resulting model is shown to replicate many of the stylized facts of financial return series and to facilitate the calculation of marginal and conditional characteristics of the model including quantile measures of risk. Estimation is carried out by adapting the exact maximum likelihood approach to the estimation of ARMA processes and the model is shown to be competitive with standard GARCH in an empirical application to Bitcoin return data.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0