Conformal prediction offers finite-sample coverage guarantees under minimal

assumptions. However, existing methods treat the entire modeling process as a

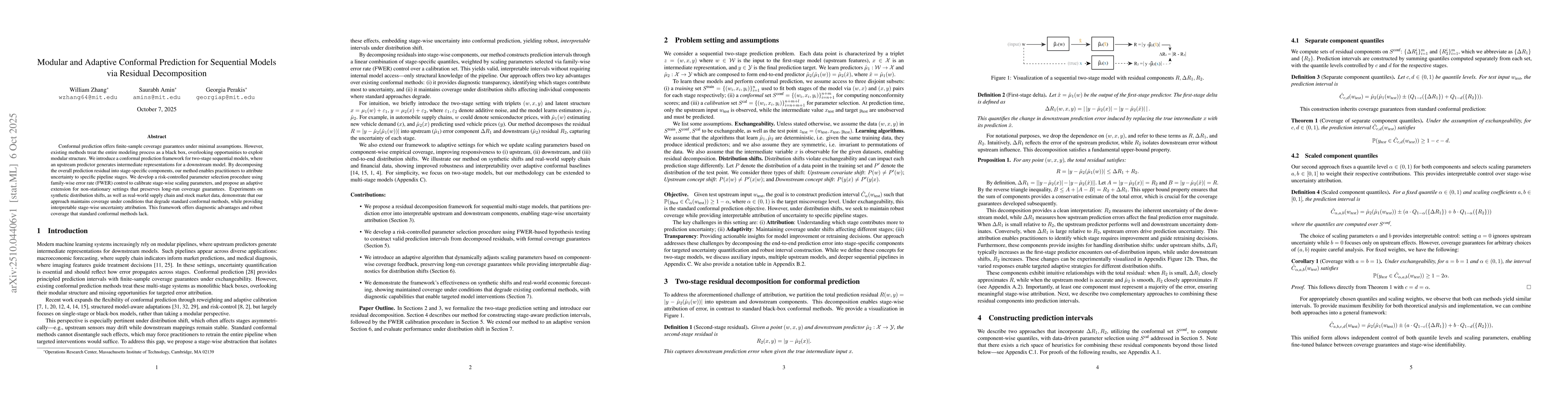

black box, overlooking opportunities to exploit modular structure. We introduce

a conformal prediction framework for two-stage sequential models, where an

upstream predictor generates intermediate representations for a downstream

model. By decomposing the overall prediction residual into stage-specific

components, our method enables practitioners to attribute uncertainty to

specific pipeline stages. We develop a risk-controlled parameter selection

procedure using family-wise error rate (FWER) control to calibrate stage-wise

scaling parameters, and propose an adaptive extension for non-stationary

settings that preserves long-run coverage guarantees. Experiments on synthetic

distribution shifts, as well as real-world supply chain and stock market data,

demonstrate that our approach maintains coverage under conditions that degrade

standard conformal methods, while providing interpretable stage-wise

uncertainty attribution. This framework offers diagnostic advantages and robust

coverage that standard conformal methods lack.

Discussion 0