Publication

Metrics

AI Quick Summary

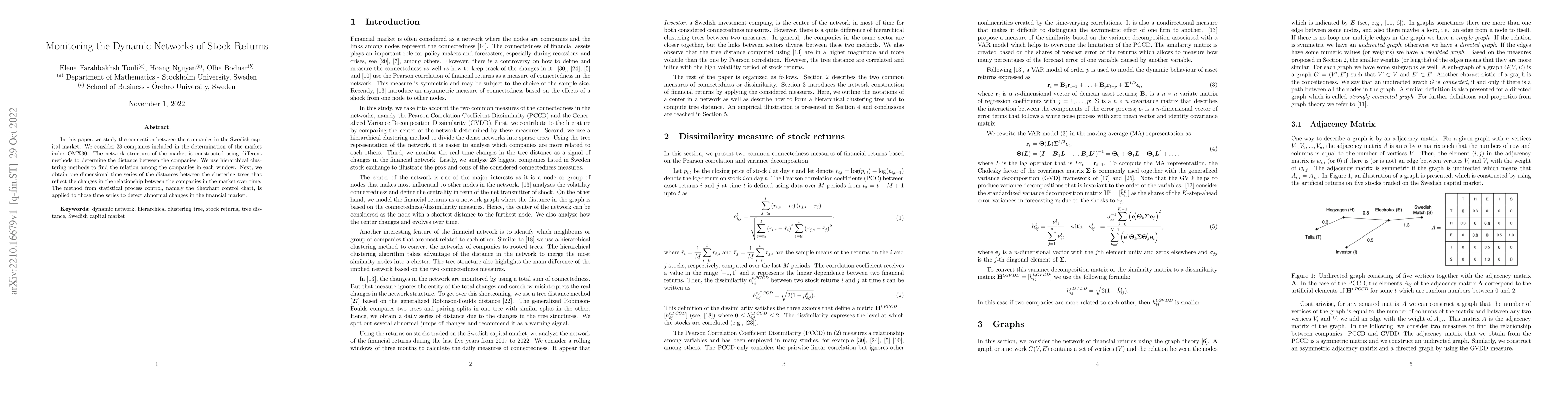

This paper constructs a network of 28 Swedish companies in the OMX30 index, using hierarchical clustering to analyze dynamic relationships over time. It employs a Shewhart control chart to detect abnormal changes in the market's relational network.

Paper Preview

Abstract

In this paper, we study the connection between the companies in the Swedish capital market. We consider 28 companies included in the determination of the market index OMX30. The network structure of the market is constructed using different methods to determine the distance between the companies. We use hierarchical clustering methods to find the relation among the companies in each window. Next, we obtain one-dimensional time series of the distances between the clustering trees that reflect the changes in the relationship between the companies in the market over time. The method of statistical process control, namely the Shewhart control chart, is applied to those time series to detect abnormal changes in the financial market.

AI Key Findings

Get AI-generated insights about this paper's methodology, results, significance, and more — seven facets brought into focus.

Impact

Paper Details

Authors

PDF Preview

Key Terms

Citation Network

Current paper (gray), citations (green), references (blue)

Display is limited for performance on very large graphs.

Discussion 0